[responsivevoice_button voice=”UK English Male”]

This course will introduce you to Self-Managed Super Funds (SMSFs), helping you understand the benefits and risks of operating an SMSF. By the end of this course, you’ll be equipped with the knowledge to decide if an SMSF is the right choice for your financial future.

Section 1: The Perks of Your Personal Super Fund

Family Superpower 👪

Combining your super with up to four to six (4-6) family members creates a larger investment pool for potentially better returns. This collective approach can amplify your investment opportunities and results.

Combining Super Funds

Strategy: Pooling resources with family members can increase your investment capital, providing more options for asset allocation. Benefits: With a larger fund, you can diversify more effectively, spreading risk across various investments.

You’re the Boss 🎩

As trustees, you and the other members have the control to make decisions that suit your specific needs and goals. This level of control can be both empowering and demanding.

Trustee Roles and Responsibilities

Governance: Trustees are responsible for managing the fund’s investments and ensuring compliance with all relevant laws and regulations. Decision-Making: Trustees make key decisions about investments, which requires a thorough understanding of the options and associated risks.

Table: Trustee Roles and Responsibilities

|

Role |

Responsibilities |

|

Trustee |

Managing investments, compliance, and reporting. |

|

Decision-Maker |

Setting and adjusting investment strategies. |

|

Record Keeper |

Maintaining accurate and thorough records. |

Investment Buffet 🍽️

An SMSF offers a wide range of investment options, including shares, ETFs, property, cryptocurrency, and more. This flexibility allows for a tailored investment strategy that aligns with your financial goals.

Investment Choices in SMSFs

Diversification: You can spread your investments across different asset classes to minimize risk. Options: From real estate to cryptocurrency, the choices are vast and varied.

Penny-Wise 💰

Running an SMSF can lead to potential cost savings, including lower fees and tax-deductible expenses. However, it is crucial to weigh these benefits against the administrative responsibilities and compliance costs.

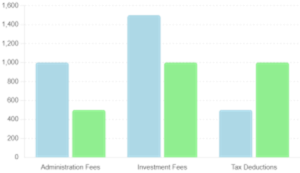

Cost Comparison with Traditional Super Funds

Fees: SMSFs can have lower ongoing fees compared to traditional super funds, particularly if your balance is substantial. Tax Benefits: SMSFs offer various tax advantages, such as deductible expenses and concessional tax rates on earnings.

Table: Cost Comparison

|

Expense Type |

Traditional Super Fund |

SMSF |

|

Administration Fees |

Higher |

Potentially Lower |

|

Investment Fees |

Higher |

Self-Managed Options |

|

Tax Deductions |

Limited |

Broader Opportunities |

Tax Tricks 📊

Smart tax planning can lead to substantial savings in an SMSF. Understanding and utilizing strategies like franking credits and capital gains tax (CGT) discounts can optimize your fund’s tax position.

Tax Planning Strategies

Franking Credits: Offsets taxes already paid by companies, reducing your overall tax liability. CGT Discounts: Long-term investments in an SMSF qualify for CGT discounts, lowering the tax on capital gains.

Fancy Finance Moves 🏄♂️

Advanced financial strategies, including derivatives, hedging, leasing commercial property, and borrowing to invest, can enhance your SMSF’s performance but also increase risk.

Advanced Investment Strategies

Derivatives and Hedging: These can protect against downside risk but require sophisticated knowledge and monitoring. Leasing and Borrowing: SMSFs can lease commercial property to members or borrow to invest under strict conditions.

Your Legacy, Your Way 🏆

Control over your super fund’s assets after your passing is a significant advantage of an SMSF. Binding nominations ensure that your super is distributed according to your wishes.

Estate Planning with SMSFs

Binding Nominations: These nominations direct how your super should be distributed and do not expire. Flexibility: You have the flexibility to change your nominations as circumstances change.

Section 2: Understanding SMSF Risks

Time is Money ⏰

Managing an SMSF requires a significant time commitment. Investment decisions, record-keeping, and compliance tasks are ongoing responsibilities that trustees must manage effectively.

Time Commitment for Managing an SMSF

Responsibilities: From daily management to long-term planning, trustees must dedicate time regularly. Efficiency Tips: Using digital tools and professional advice can help streamline management tasks.

Size Matters 📏

Having a sufficient super balance is crucial for making an SMSF cost-effective. Generally, a balance of at least $200,000 is recommended to justify the costs and effort involved.

Cost-Effectiveness of SMSFs

Balance Thresholds: A larger balance can spread fixed costs over a more significant amount, making the SMSF more efficient. Sustainability: Ensure that your SMSF has enough assets to remain viable over the long term.

Table: Recommended Balance Thresholds

|

Super Balance ($) |

Cost-Effectiveness |

|

< 200,000 |

Less Cost-Effective |

|

200,000 – 500,000 |

Moderately Cost-Effective |

|

> 500,000 |

Highly Cost-Effective |

Rules, Rules, Rules 📚

SMSFs are subject to strict legal requirements, and non-compliance can result in severe penalties. Understanding these obligations is essential for any trustee.

Legal Obligations and Compliance

Governance: Trustees must ensure the fund complies with all regulations, including financial reporting and investment restrictions. Penalties: Failure to comply with legal requirements can result in fines and other penalties from regulatory authorities.

Home Sweet Home? 🏠

Residency criteria must be met for SMSFs to receive tax benefits. Trustees must ensure that the central management and control of the fund are in Australia, and the majority of fund members reside in Australia.

Residency Rules for SMSFs

Criteria: The fund’s central management and control must be in Australia, and most members should reside in Australia. Tax Implications: Non-compliance with residency rules can result in losing tax concessions and facing additional taxes.

Table: Residency Rules

|

Criteria |

Requirement |

|

Central Management and Control |

Must be in Australia |

|

Fund Members |

Majority must reside in Australia |

|

Active Member Test |

Satisfied if member contributions are limited |

Financial Savvy Required 🧠

A good understanding of investments and finance is crucial for managing an SMSF successfully. Continuous education and staying informed about market trends and regulations are essential.

Financial Knowledge Requirements

Essential Skills: Trustees should understand investment principles, financial markets, and regulatory requirements. Continuous Learning: Regularly updating your knowledge through courses, seminars, and professional advice is critical.

No Safety Net 🕸️

Unlike other super funds, SMSFs do not have government compensation for fraud or theft. Trustees must implement robust risk management and protection measures.

Risk Management

Fraud and Theft: Implementing security measures and conducting regular audits can help protect your fund. Protection Measures: Ensure compliance with best practices for security and risk management.

DIY Dispute Resolution ⚖️

SMSFs must resolve disputes internally, as they do not have access to the Superannuation Complaints Tribunal. Understanding your options for dispute resolution is crucial.

Dispute Resolution Options

Internal Resolution: Attempt to resolve conflicts within the fund

Section 3: Weighing the Pros and Cons

Comparing Benefits and Risks

|

Category |

Benefits |

Risks |

|

Control |

Customizable rules, strategic decisions |

Significant time investment required |

|

Investments |

Diverse options, including unique assets |

Requires investment knowledge |

|

Cost |

Potentially lower fees, tax-deductible |

Can be expensive for smaller funds |

|

Planning |

Greater control over estate distribution |

No government compensation for losses |

|

Borrowing |

Limited recourse borrowing allowed |

Complex rules, potential for high penalties |

Conclusion: Making the Decision

Running an SMSF can be rewarding, but it’s not for everyone. It requires time, knowledge, and careful consideration of your financial situation. Before deciding, ask yourself:

- Do I have enough super to make an SMSF cost-effective?

- Am I comfortable with the legal responsibilities?

- Do I have the time and expertise to manage investments?

- Have I considered seeking professional advice?

Remember, there’s no one-size-fits-all in super. Whether an SMSF is right for you depends on your unique circumstances and goals.

References and Additional Links

-

- Australian Taxation Office (ATO) SMSF information: ATO SMSF Guide

- ASIC’s MoneySmart SMSF Guide: MoneySmart SMSF Guide