SMSF Administration and Reporting Obligations

What Laws, rules apply to the ongoing management of SMSFs by the ATO and the super and tax laws that govern SMSFs. we will cover these points in this lesson

[responsivevoice_button voice=”UK English Male”]

Trustees’ Responsibilities in SMSF Administration

Trustees are responsible for the ongoing administration of their SMSF, including:

- Meeting Annual Compliance Obligations: Preparing and lodging annual returns, conducting audits, and maintaining accurate records.

- Maintaining Accurate Records: Detailed guidance on what records need to be kept (financial statements, member reports, tax documents) and for how long.

- Managing Changes in Members’ Circumstances: Such as death, separation, divorce, or deciding to wind up the SMSF.

- Winding Up the SMSF if Necessary: Following prescribed steps to close the fund.

In the event of significant changes, trustees should seek professional advice to ensure compliance with superannuation laws.

Annual Obligations

- Compliance: Ensuring that all operations adhere to the sole purpose test and other legislative requirements.

- Record Keeping: Detailed guidance on necessary records (financial statements, member reports, tax documents) and retention periods.

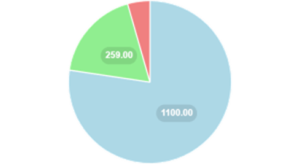

Fee Structure

|

Fee Type |

Amount (AUD) |

Description |

|

My SMSF Administration Fee |

$1,100 pa* |

Includes tax, audit, and support |

|

ATO Levy |

$259 |

Annual levy charged by the Australian Tax Office |

|

ASIC Company Renewal Fee |

$63 |

For a special purpose company |

*Note: The administration fee may be subject to changes due to CPI and other factors.

Role of the Australian Taxation Office (ATO)

The ATO serves as the primary regulatory authority for SMSFs, focusing on:

- Compliance Enforcement: Ensuring adherence to superannuation rules, legislation, and regulations.

- Resource Provision: Providing documentation to aid in the establishment and ongoing administration of SMSFs.

- Law Enforcement: Taking action against breaches of superannuation laws.

- Auditor Oversight: Ensuring SMSF auditors perform to required standards.

Managing Significant Changes in SMSF Circumstances

Member’s Death

- Procedure: The SMSF trust deed and any binding death benefit nominations guide the distribution of the deceased member’s superannuation balances.

- Distribution: Funds are transferred to nominated beneficiaries or directed to the member’s estate.

Separation or Divorce

- Procedure: Superannuation assets may need to be split as part of the property settlement.

- Trust Deed Review: Ensure the SMSF trust deed reflects the current structure of the fund.

Winding Up the SMSF

- Procedure: Follow steps including liquidating assets, settling outstanding taxes and expenses, and distributing remaining funds.

- Distribution Options: Funds can be distributed to members or rolled over into other complying superannuation funds.

Seeking Professional Advice

- Importance: Ensures compliance with superannuation laws and helps trustees make informed decisions.

Event Impact and Recommended Actions

|

Event |

Impact on SMSF |

Recommended Action |

|

Death |

Distribution of member’s balance per trust deed and nominations |

Ensure nominations are up-to-date and in line with estate planning. |

|

Separation/Divorce |

Potential split of superannuation assets |

Review and possibly amend the trust deed. |

|

Winding Up |

Liquidation of all fund assets and closure of the SMSF |

Follow legal procedures for asset liquidation and fund distribution. |

Role of ASIC

The Australian Securities and Investments Commission (ASIC) monitors SMSF auditors, ensuring they meet professional standards and regulatory requirements, thereby enhancing SMSF integrity and compliance.