[responsivevoice_button voice=”UK English Male”]

Understanding SMSF Benefit Payments:

Understanding the rules and conditions surrounding benefit payments from an SMSF (Self-Managed Superannuation Fund) is crucial for both trustees and members. This lesson will cover the conditions of release, payment types, and tax implications of benefit payments.

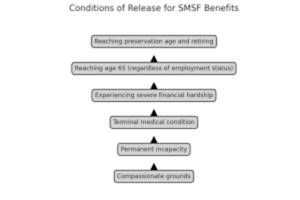

Conditions of Release

|

Condition of Release |

Description |

|

Reaching Preservation Age and Retiring |

Members can access their benefits upon reaching their preservation age and retiring. |

|

Reaching Age 65 |

Members can access their benefits regardless of their employment status. |

|

Severe Financial Hardship |

Members experiencing severe financial hardship can access their benefits. |

|

Terminal Medical Condition |

Members diagnosed with a terminal medical condition can access their benefits. |

|

Permanent Incapacity |

Members who are permanently incapacitated can access their benefits. |

|

Compassionate Grounds |

Members can access their benefits on specific compassionate grounds. |

Note: Preservation age ranges from 55 to 60, depending on the member’s date of birth.

Payment Types

Once a condition of release is met, benefits can be paid as:

Lump Sum

- Single Payment: Withdraws a portion or all of the member’s account balance.

- Payment Methods: Can be paid in cash or as an in-specie transfer of assets.

⬇️

Account-Based Pension

- Regular Payments: Drawn from the member’s account balance.

- Minimum Annual Payment: Required based on the member’s age and account balance.

- No Maximum Annual Payment: Except for Transition to Retirement pensions.

⬇️

Combination of Both

- Flexible Payments: Members can choose to receive a combination of lump sum and pension payments.

Once a condition of release is met, benefits can be paid as:

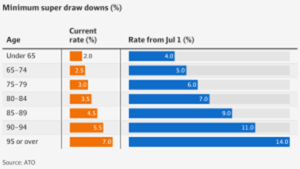

Minimum Annual Pension Payments

For account-based pensions, minimum annual payment requirements apply based on the member’s age.

Tax Implications

Lump Sum Benefits

- Tax-Free Component: Not taxed.

- Taxable Component (Taxed Element): Taxed at concessional rates up to preservation age, tax-free after age 60.

- Taxable Component (Untaxed Element): Taxed at higher rates.

Pension Payments

- Members Aged 60 and Over: Pension payments are generally tax-free.

- Members Under 60: The taxable portion of pension payments is taxed at the member’s marginal tax rate, less a 15% tax offset.

Recordkeeping

Trustees must maintain accurate records of all benefit payments made, including:

- Date of Payment

- Payment Type: Lump sum or pension.

- Amount Paid

- Recipient Details

- Tax Components: Tax-free and taxable.

These records are essential for accurate reporting and compliance with ATO requirements.

Additional Resources

- ATO – SMSF Benefit Payments: ATO SMSF Benefit Payments

- ASIC – SMSF Pension and Lump Sum Payments: ASIC SMSF Pensions and Lump Sum Payments

By understanding the rules and tax implications of benefit payments, SMSF trustees and members can make informed decisions about accessing their superannuation benefits while ensuring compliance with relevant regulations. Understanding the rules and conditions surrounding benefit payments from an SMSF is crucial for both trustees and members. This lesson will cover the conditions of release, payment types, and tax implications of benefit payments.