[responsivevoice_button voice=”UK English Male”]

Understanding SMSF Contribution Rules

Understanding the rules governing contributions to your SMSF is essential for effective management and compliance. This lesson covers the types of contributions, contribution caps, and eligibility criteria.

Types of Contributions

There are three main types of contributions that can be made to an SMSF:

|

Type |

Details |

|

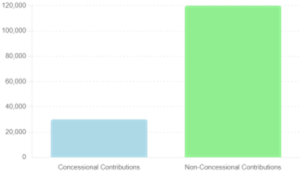

Concessional Contributions (CCs) |

$32,500 – 2026-27FY |

|

Non-Concessional Contributions (NCCs) |

$130,000 – 2026-27FY |

|

Other Contributions |

Spouse Contributions: Contributions made on behalf of a low-income or non-working spouse, which may entitle the contributing spouse to a tax offset of up to $540 (18% of the first $3,000 contributed). |

Contribution Caps

Annual caps apply to both concessional and non-concessional contributions. These caps are indexed periodically and are as follows for the 2026-27 financial year:

Note: The bring-forward rule allows eligible individuals to make up to three years’ worth of NCCs in a single year (up to $390,000 for 2026-27). Exceeding these caps may result in additional taxes and penalties:

- Excess CCs are taxed at the member’s marginal tax rate, with an excess contributions charge applied.

- Excess NCCs may be withdrawn from the fund, with associated earnings taxed at the member’s marginal tax rate.

Eligibility Criteria

Age Restrictions:

- Under 67: No restrictions on contributing.

- 67 to 74: Voluntary contributions can be made without meeting the work test, however the work test (or work test exemption) must be met to claim a tax deduction for personal contributions.

- 75 and over: Only mandated employer contributions (e.g., SG) can be accepted.

Work Test:

- To meet the work test, a member must be gainfully employed for at least 40 hours in a consecutive 30-day period during the financial year.

- The work test exemption allows eligible individuals to make voluntary contributions for an additional 12 months after the end of the financial year in which they last met the work test.

Acceptance of Contributions

SMSF trustees must ensure that contributions are only accepted when the following conditions are met:

- The fund’s trust deed allows for the acceptance of the contribution type.

- The member is eligible to make the contribution based on age and work test requirements.

- The contribution does not exceed the relevant cap.

Recordkeeping

Trustees must maintain accurate records of all contributions received, including:

- Date of receipt

- Contribution type (CC, NCC, or other)

- Amount contributed

- Contributor details (e.g., employer, member, spouse)

These records are essential for accurate reporting and compliance with ATO requirements.

Additional Resources

-

- ATO – SMSF Contributions: ATO SMSF Contributions

By understanding and adhering to the contribution rules, SMSF trustees can ensure their fund remains compliant while effectively managing member contributions and working towards their retirement goals.