Leveraging the Proposed FHSS Scheme Increase to $60,000: A Strategic Guide for My SMSF Members For members of self-managed super funds (SMSFs), the First Home Super Saver Scheme (FHSS) presents a unique opportunity to utilize superannuation for purchasing a first home. The Australian government’s recent budget 2024 proposal to increase the maximum releasable amount under […]

Leveraging the Proposed FHSS Scheme Increase to $60,000: A Strategic Guide for My SMSF Members

For members of self-managed super funds (SMSFs), the First Home Super Saver Scheme (FHSS) presents a unique opportunity to utilize superannuation for purchasing a first home. The Australian government’s recent budget 2024 proposal to increase the maximum releasable amount under the FHSS from $30,000 to $50,000 starting 1 July 2024 could significantly enhance this opportunity. This change is tailored to aid SMSF members in boosting their first home deposits while taking advantage of the concessional tax treatment offered by the super system.

Overview of the FHSS for SMSF Members

The FHSS allows SMSF members to save for their first home within their super fund, leveraging the low-tax environment:

- Contributions: Members can make voluntary concessional and non-concessional contributions to their SMSF that can later be withdrawn to finance their first home purchase.

- Tax Benefits: These contributions benefit from a concessional tax rate of 15%, significantly lower than typical personal income tax rates.

- Withdrawals: With the proposed changes, up to $50,000 of these contributions, along with associated earnings, can be withdrawn for a first home purchase from 1 July 2024.

Strategic Implications of the $50,000 FHSS Increase for SMSF Members

- Maximizing Contributions

To optimize the benefits of the FHSS, SMSF members should consider strategies to maximize their voluntary contributions within the new $50,000 limit. Planning to contribute strategically over the years leading up to the home purchase can significantly increase the deposit size. For couples, each partner can withdraw $50,000 from their respective SMSFs, potentially pooling $100,000 towards their home.

- Tax Planning and SMSF Compliance

Utilizing the FHSS requires careful tax planning and compliance with SMSF regulations. Members must ensure that their contributions do not exceed the superannuation caps and that all SMSF activities align with the sole purpose test of superannuation—to provide retirement benefits. Consulting with a specialist in SMSF tax advice is crucial to navigate these requirements effectively.

- Timing and Coordination of Withdrawals

Coordinating the timing of FHSS withdrawals with the home purchase process is essential. SMSF trustees must manage fund liquidity to ensure that funds are available when needed for the property purchase, without disrupting the fund’s investment strategies.

- Selecting Appropriate Investments within the SMSF

Investment decisions within the SMSF should consider the timing and objectives of the FHSS. Since the funds will be withdrawn for a home purchase, the investment strategy might lean towards more liquid or lower-risk investments as the withdrawal date approaches.

Case Study: A Tailored Strategy for an SMSF Member

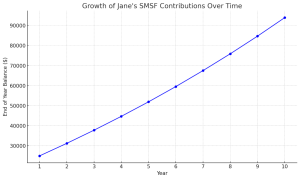

Consider Jane, a 30-year-old professional planning to purchase her first home within the next five years. She is a member of an SMSF and earns $90,000 annually. Her strategy involves:

- Annual Contributions: Contributing $10,000 yearly to her SMSF for five years.

- Tax Savings: Capitalizing on the lower tax rate for contributions, which reduces her tax liability while growing her savings more efficiently.

| Year | Annual Contribution | Total Contributions | Interest Earned | End of Year Balance |

| 1 | $5,000 | $25,000 | $0.00 | $25,000.00 |

| 2 | $5,000 | $30,000 | $1,250.00 | $31,250.00 |

| 3 | $5,000 | $35,000 | $1,562.50 | $37,812.50 |

| 4 | $5,000 | $40,000 | $1,890.63 | $44,703.13 |

| 5 | $5,000 | $45,000 | $2,235.16 | $51,938.28 |

| 6 | $5,000 | $50,000 | $2,596.91 | $59,535.20 |

| 7 | $5,000 | $55,000 | $2,976.76 | $67,511.96 |

| 8 | $5,000 | $60,000 | $3,375.60 | $75,887.55 |

| 9 | $5,000 | $65,000 | $3,794.38 | $84,681.93 |

| 10 | $5,000 | $70,000 | $4,234.10 | $93,916.03 |

- Investment Strategy: Her SMSF invests these contributions in a balanced mix of assets, planning for liquidity and stability as the withdrawal date nears.

By the time Jane is ready to purchase her home, she can withdraw up to $50,000 plus earnings from her SMSF under the FHSS, significantly bolstering her purchasing power.

Conclusion

For My SMSF members, the proposed increase in the FHSS withdrawal cap to $50,000 is a substantial enhancement that can aid significantly in securing a first home. It’s crucial for members to plan their contributions carefully, remain compliant with SMSF regulations, and maintain a flexible but strategic investment approach within their fund. Regular consultations with financial and SMSF advisors will ensure that members can maximize the advantages of the FHSS without compromising their fund’s compliance and performance.

ADDITIONAL INFORMATION:

Contact My SMSF – Contact Us | SMSF Setup, SMSF Accounting and SMSF Loans (mysmsfproperty.com.au)

ATO SMSF Setups –