A self-managed super fund allows Australians, to take greater control over their retirement savings. Investing in property within a SMSF has been an accepted strategy since the super laws changed in 2006, and the ability to earn rental income and capital growth from an asset that keep up with inflation makes buying residential property through […]

A self-managed super fund allows Australians, to take greater control over their retirement savings. Investing in property within a SMSF has been an accepted strategy since the super laws changed in 2006, and the ability to earn rental income and capital growth from an asset that keep up with inflation makes buying residential property through an SMSF a very popular strategy. In this comprehensive guide, we will cover everything that you need to know to purchase a residential property through your SMSF and staying compliant.

1. Pre-Requisites for Property Investment via SMSF

Before purchasing property through your SMSF, make sure you have the following in place:

| Requirement | Description |

| SMSF Setup | Fund must have individual or corporate trustees. |

| SMSF Available Funds | $150,000 – $200,000 including contributions to the SMSF from one or members |

| Investment Strategy | Must align with property investment and retirement benefits. |

| Sufficient Funds | 30-40% deposit required for loans; enough liquidity for expenses. |

| Compliance with Sole Purpose | The property must benefit members solely for retirement purposes and cannot be used to gain a present-day benefit. |

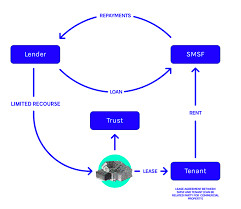

2. Limited Recourse Borrowing Arrangements (LRBA)

If your SMSF needs to borrow, it must do so under a Limited Recourse Borrowing Arrangement (LRBA). This ensures the lender only has a claim on the property tied to the loan, safeguarding other SMSF assets. The property will be held in a bare trust during the loan term.

| Feature | Description |

| Loan Structure | Only the property can be seized if the loan defaults. |

| Deposit Requirements | Typically, 20% -3 0% of the property value. |

| Interest Rates | SMSF loan rates range from 6.99% – 8.50% |

| Loan Approval | Only specialized lenders offer SMSF loans. |

3. The Role of Bare Trusts and Trustees

A bare trustee holds the legal title of the property whilst the bare trust document serves as the proof of the arrangement between the SMSF and the Bare Trustee. The SMSF retains beneficial ownership, with no direct debt associated with the fund, which ensures compliance with super laws.

| Bare Trust Structure | Function |

| Bare Trustee (Legal Owner) | Holds the legal title to the property during the loan period. |

| SMSF (Beneficial Owner) | Receives rental income and capital growth benefits. |

| Title Transfer After Loan Repayment | Property title transfers to SMSF without triggering stamp duty* |

*Important: Ensure the contract is signed correctly by the bare trustee to avoid double stamp duty with the deed stamped by the Office of State Revenue in the applicable state. Failing to follow the proper execution sequence could result in significant additional costs.

4. Correct Contract Execution to Avoid Double Duty

The correct sequence for executing the property purchase contract is critical:

-

- Bare Trustee signs the purchase contract as the legal buyer.

-

- Loan agreements and documentation are finalised.

-

- Bare Trustee holds legal ownership until the loan is repaid.

-

- After repayment, title transfers to the SMSF without stamp duty*.

5. Steps to Buying Residential Property with SMSF

| Step | Details |

| Identify the Property | Research properties aligned with your SMSF strategy. Consider rental yield and capital growth. |

| Work with Experts | Engage My SMSF for administration, legal document setup, and referral assistance. |

| Establish a Bare Trust | Create a bare trust to hold the property on behalf of your SMSF. |

| Apply for an SMSF Loan | Secure a loan with a lender specialising in SMSF borrowing. |

| Execute Contract Properly | Ensure the bare trustee signs the contract to avoid double duty. |

| Complete Settlement | Manage legal documents and transfer the title to the bare trust. |

| Manage Rent and Expenses | All rental income and expenses must flow through to the SMSF account. |

6. Compliance Requirements and Ongoing Management

Rental Income Management:

-

- All rental income must be deposited directly into the SMSF’s bank account.

-

- Property-related expenses such as repairs, rates, and insurance must be paid from the SMSF account.

Annual Reporting and Audit:

-

- Annual audits are required to ensure compliance with ATO regulations.

-

- Property valuations must be conducted regularly for accurate reporting.

-

- A property title report is now required to check the parties to the arrangement are compliant and the level of debt associated.

7. Benefits and Risks of Buying Residential Property through SMSF

| Benefits | Risks |

| Tax Advantages: Rental income taxed at 15%; 0% during pension phase. | Liquidity Constraints: Property is an illiquid asset. |

| Control Over Investments: Trustees manage the property. | Higher Loan Costs: Interest rates are higher for SMSF loans. |

| Estate Planning Benefits: Assets are transferred smoothly to beneficiaries. | Compliance Risks: Breaches can result in penalties or fund disqualification. |

8. Relevant SIS Act Sections Governing Property Investments

To ensure compliance, your SMSF must adhere to the following provisions from the Superannuation Industry (Supervision) Act 1993 (SIS Act):

| Section | Description |

| Section 62 – Sole Purpose Test | Property must provide retirement benefits only. |

| Section 66 – Acquisition from Related Parties | SMSF cannot acquire residential property from related parties. |

| Section 67A & 67B – LRBA | Sets rules for borrowing arrangements within an SMSF. |

| Section 71 – In-House Assets | Limits exposure to related party assets to 5% of total assets. |

| Section 109 – Arm’s Length Rules | All transactions must be at market value. |

10. How My SMSF Can Help You

At My SMSF, we specialise in helping SMSF trustees navigate the complexities of property investment. Our expert services include:

-

- Bare trust documents: We establish compliant structures for property purchases.

-

- SMSF setup and ongoing administration: We work with lenders to secure the best terms for your fund.

-

- Compliance management: We ensure your fund meets all ATO requirements and stays audit ready.

-

- Lending Referrals: we can refer you to a suitable lender and using our calculators and tools which assist you make informed decisions.

12. Conclusion: How Property Investment Can Unlock Your Retirement Wealth

Investing in residential property through your SMSF provides a unique opportunity to access the most popular investment asset for Australian wealth creation via an SMSF. It further has the potential to add to the members retirement returns via future rental income and capital gains. The proper execution of legal structures such as bare trust setups and compliance with the super laws such; which could easily result in costly mistakes, including double stamp duty; will ensure your fund is compliant.

Additional Resources:

ATO SMSF Property – Click for more details

Contact My SMSF – Click here

Always seek professional financial, tax and legal advice with SMSF property strategies.