Limited Recourse Borrowing Arrangements (LRBAs), also referred to as SMSF loans or super fund loans, have long been a topic of debate in the Australian SMSF sector.

By R.J.

Limited Recourse Borrowing Arrangements (LRBAs), also referred to as SMSF loans or super fund loans, have long been a topic of debate in the Australian SMSF sector. As the 2025 political climate evolves, there is increasing speculation about potential reforms or bans on LRBAs. Given property constitutes an estimated 60% of Australians’ collective wealth, any changes could significantly impact SMSF trustees and property investors. This article delves into the political context, reform likelihood, and implications for SMSFs.

1. What Are LRBAs?

LRBAs, also known as SMSF loans, allow SMSFs to borrow funds for purchasing a single asset, typically property, while limiting the lender’s recourse to that asset alone. This structure can magnify investment returns during strong property markets but equally increases risks during downturns or in a climate of rising interest rates.

LRBA Risks and Rewards

| Benefits | Risks |

| Amplified capital growth | Potential for eroded fund balances |

| Leverage for property investments | Mounting debt with market or rate changes |

| Stable long-term returns (historically) | Increased compliance obligations |

2. Political Parties’ Stance on LRBAs

| Party | Stance on LRBAs | Likelihood of Reform |

| Labor Party | Advocates tighter restrictions or an outright ban to curb property inflation risks. | Moderate to High |

| Liberal–National Coalition | Supports financial autonomy; prefers targeted measures rather than full bans. | Low to Moderate |

| The Greens | Favors banning LRBAs to improve housing affordability. | High |

Labor’s Perspective

“LRBAs increase systemic risks and inflate property values, affecting housing affordability for younger Australians.”

Coalition’s Balancing Act

“Leverage in superannuation must balance economic freedom with prudent financial management.”

3. Drivers Behind Potential Bans

Several factors influence the possibility of banning or restricting LRBAs, or SMSF loans:

Key Drivers of Reform

| Driver | Impact |

| Housing affordability | Restricting LRBAs may reduce speculative pressure on property. |

| Debt levels and systemic risk | High property debt could jeopardize retirement savings. |

| Regulatory scrutiny | Regular reviews highlight risks of excessive super leverage. |

4. Implications for SMSFs

4.1 Reduced Access to Property

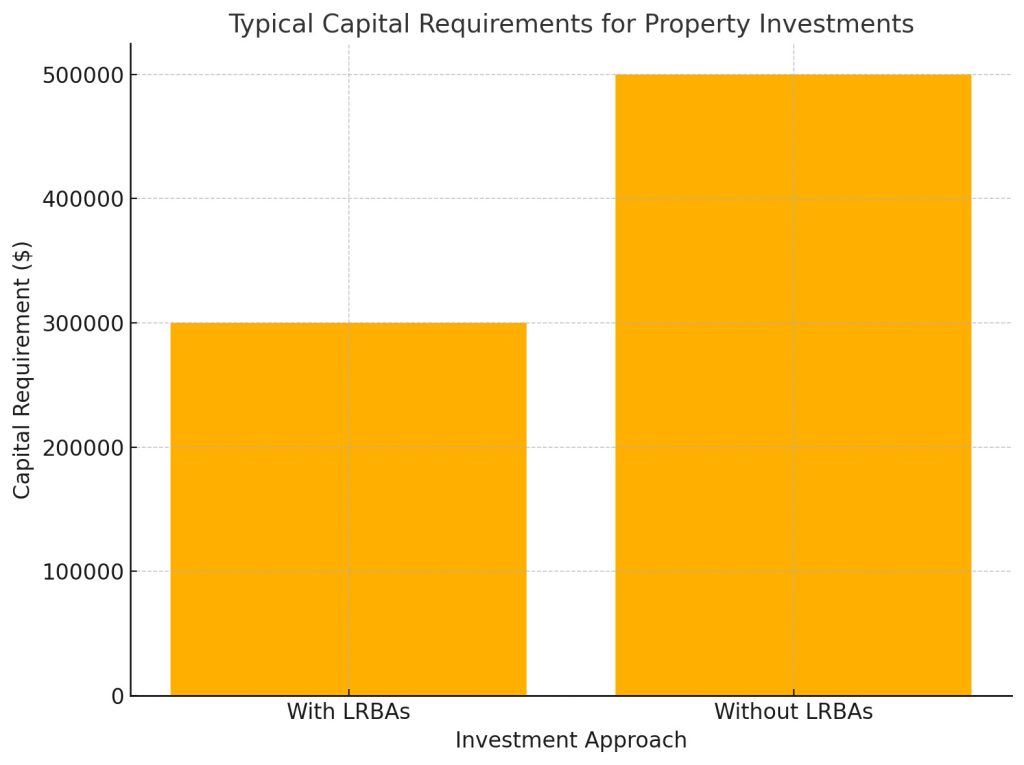

Many SMSFs rely on super fund loans to invest in property. A ban would necessitate higher capital reserves, making direct property investments less accessible.

Chart: Typical Capital Requirements for Property Investments With and Without LRBAs

4.2 Shift in Investment Strategies

Restrictions could push SMSFs toward alternative investments, such as:

- Listed Real Estate Investment Trusts (REITs)

- Infrastructure funds

- High-yield debt instruments

4.3 Potential Impact on Property Markets

A ban could slightly ease property price pressures in SMSF-heavy segments, particularly in suburban and metropolitan areas.

Table: SMSF-Driven Demand in Key Property Markets

| Region | Share of SMSF Investments (%) | Projected Impact of LRBA Ban |

| Metropolitan Areas | 35% | Moderate decline in demand |

| Regional Areas | 25% | Minimal impact |

5. Likelihood of LNC Intervention

The Liberal–National Coalition remains less likely to endorse a full LRBA ban. However, targeted reforms could include:

Proposed LNC Measures

| Measure | Details |

| Targeted Caps | Capping SMSF borrowings proportional to fund balances. |

| Serviceability Tests | Strengthened borrowing and repayment assessments. |

| Gradual Phase-Out | Phased removal of LRBAs to minimize market disruption. |

6. Preparing for Change

Actionable Steps for SMSF Trustees

| Step | Details |

| Review leverage strategies | Evaluate debt levels and property market exposure. |

| Consider alternative investments | Explore REITs, infrastructure funds, and diversified assets. |

| Stay compliant | Monitor regulatory updates and adapt quickly. |

Conclusion: A Pivotal Moment for SMSFs

The future of LRBAs, or SMSF loans, hangs in the balance as policymakers weigh financial risks against investment freedoms. For SMSF trustees, staying informed and proactively managing leverage is key to navigating this uncertain landscape along with seeking advice when necessary. Whether reforms lead to stricter caps or outright bans, understanding the potential impact on your fund is essential to ensuring long-term retirement success. We hope you find this article informative and preparative should this measure eventuate.

Need expert guidance on your SMSF?

Explore our tailored SMSF accounting and compliance services at My SMSF Property

Disclaimer: This article is intended as general information only. Seek advice regarding all SMSF loans and the potential for future legislative changes that may impact your SMSF. This article highlights a potential risk of SMSF loan changes, that is being debated at present.