A Comprehensive Guide to Buying Property through a Self-Managed Super Fund (SMSF) Introduction Self-Managed Super Funds (SMSFs) are becoming increasingly popular for Australians to manage their superannuation. One of the advantages of using an SMSF is the ability to invest in property directly. However, the process can be complex due to recent changes in bank […]

A Comprehensive Guide to Buying Property through a Self-Managed Super Fund (SMSF)

Introduction

Self-Managed Super Funds (SMSFs) are becoming increasingly popular for Australians to manage their superannuation. One of the advantages of using an SMSF is the ability to invest in property directly. However, the process can be complex due to recent changes in bank and lender credit conditions and requirements, as well as modifications to the stamping of bare trust deeds.

This article provides a comprehensive five-step guide to purchasing property within an SMSF, incorporating these recent changes.

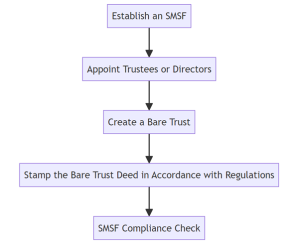

- Setting Up the SMSF and Bare Trust

Key Points:

- An SMSF can have between one to six members.

- Each member will be a trustee or director responsible for managing the SMSF.

- A Bare Trust arrangement is necessary for purchasing property.

- Ensure the Bare Trust deed is stamped by the relevant state or territory revenue office according to the new regulations.

- Formulate an Investment Strategy

Investment Strategy Checklist:

- Align Objectives and Risk Profiles: Ensure the strategy aligns with fund members’ objectives and risk profiles.

- Specify Property Purchase Intentions: The strategy should clearly outline the intention to purchase property.

- Sole Purpose Test Compliance: The property investment must meet the ‘sole purpose test’ to provide retirement benefits to fund members.

- Loan Pre-Approval and Property Selection

Lender Considerations:

- Lenders typically lend a maximum of 60-80% of the property’s value.

- Loans are subject to postcode assessment, SMSF income streams (super contributions, rental income, interest), and serviceability.

Property Selection Requirements Table:

Criteria | Requirements |

Sole Purpose Test | Must provide retirement benefits to SMSF members. |

Investment Strategy | Should align with the formulated investment strategy. |

Loan Pre-Approval | Ensure the property meets lender credit requirements. |

Risk Management | Assess the risk profile of the property. |

- Property Purchase and Loan Finalization

Important Details:

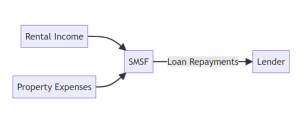

- The Bare Trust holds the property title.

- The SMSF makes loan repayments, receives rental income, and manages expenses.

- While the loan is in place, significant improvements to the property are prohibited.

- Ongoing Management

Ongoing Management Checklist:

- Review Investment Strategy Regularly: Adjust the strategy as required to reflect the SMSF’s changing goals and market conditions.

- Ensure Regulatory Compliance: Adhere to all SMSF regulations, including tax laws.

- Meet Loan Repayments and Property Expenses: Maintain a steady cash flow to manage loan and property costs.

Staying Up to Date

- Legislative Changes: Stay informed about new rules, like the altered stamping process for Bare Trust deeds.

Conclusion

Buying property through an SMSF can be an effective way to grow your super and potentially provide strong returns. However, it requires careful management and adherence to evolving lender requirements and super and tax laws. Following this guide will help ensure a smooth and compliant process for purchasing property within your SMSF.

Summary Table

Step | Key Actions |

1. Setup SMSF/Bare Trust | Establish SMSF, appoint trustees, and create a Bare Trust. |

2. Investment Strategy | Formulate a strategy aligned with fund member objectives. |

3. Loan Pre-Approval | Secure pre-approval and select a property. |

4. Property Purchase | Finalise the loan and complete the purchase. |

5. Ongoing Management | Review strategy, manage finances, and remain compliant. |