SMSF Property Buyer’s Journey: A Comprehensive Guide Introduction This comprehensive guide outlines the SMSF property buyer’s journey, focusing on setting up a Self-Managed Super Fund (SMSF) and the key considerations involved. We’ll explore SMSF setup, loan options, lender criteria, postcode screening, and annual tax obligations, empowering you to navigate the SMSF property process confidently. 1. […]

SMSF Property Buyer’s Journey: A Comprehensive Guide

Introduction

This comprehensive guide outlines the SMSF property buyer’s journey, focusing on setting up a Self-Managed Super Fund (SMSF) and the key considerations involved. We’ll explore SMSF setup, loan options, lender criteria, postcode screening, and annual tax obligations, empowering you to navigate the SMSF property process confidently.

1. Setting Up an SMSF

| Item | Details |

|---|---|

| Setup Fee | $990 (including trustee company, bank account, ABN, TFN) |

| Time to Establish | 2-6 weeks |

| Annual Fee | $1,100 (tax and audit services) |

| Included Services | Fund deed, tax filing, and ongoing support |

Key Benefits:

- Control and flexibility in investment decisions (property, gold, Bitcoin).

- Improved estate planning and succession flexibility.

- Autonomy over retirement savings by becoming a trustee and fund manager.

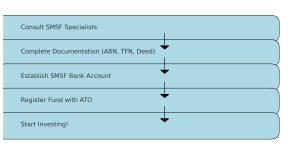

SMSF Setup Process Flow

2. Selecting Lenders for SMSF Loans

Bank vs. Non-Bank Lenders

| Type | Examples | Pros | Cons |

|---|---|---|---|

| Bank Lenders | Select major banks | Established reputation | Stricter eligibility criteria |

| Non-Bank Lenders | Liberty Finance, Loans.com.au | Flexible lending criteria | Higher interest rates, limited offers |

Note: Many banks no longer offer SMSF loans except for select existing customers. Non-bank lenders provide more tailored options for SMSF borrowers.

3. Assessing Loan Servicing Capacity

Lenders assess several factors to ensure the SMSF can service the loan effectively.

| Loan Servicing Factors | Description |

|---|---|

| Rental Income | Income generated from property investments. |

| Super Contributions | Ongoing contributions by SMSF members. |

| Loan-to-Value Ratio (LVR) | Percentage of loan compared to property value. |

| Additional Contributions | Voluntary deposits to meet loan servicing needs. |

Expert Tip: Engage an SMSF finance broker early to evaluate your capacity for loan servicing. This helps avoid roadblocks during the fund setup phase.

4. Postcode Screening for SMSF Property Investments

Postcode screening plays a crucial role in evaluating the potential of an investment property.

| Property Factors | Why It Matters |

|---|---|

| Growth Potential | Higher returns on investment over time. |

| Rental Demand | Consistent cash flow through tenants. |

| Market Stability | Minimizes risks during market downturns. |

Lenders’ Role in Postcode Screening:

Lenders use postcode screening to assess property value stability and minimize their risk. Properties in volatile areas may lead to loan rejections or stricter terms.

5. Annual Tax and Audit Obligations

Documents Required for Annual Reporting:

| Document | Purpose |

|---|---|

| Contract of Sale | Proof of property purchase |

| Property Rental Report | Summary of rental income |

| Property Valuation | Assessed property value for tax purposes |

| Bank and Loan Statements | Track fund transactions and repayments |

| Depreciation Schedule | Helps maximize tax deductions |

Audit Requirements

SMSFs undergo annual audits to ensure compliance with regulatory standards.

| Audit Requirement | Details |

|---|---|

| Independent Auditor | Ensures compliance and financial transparency. |

| Bare Trust Documents | Reviewed as part of SMSF property compliance. |

| Investment Strategy Updates | Mandatory annual updates as per audit rules. |

6. SMSF Property Buyers Checklist

Here’s a step-by-step checklist to guide you through the process:

Research and Consultation:

- Decide if an SMSF suits your investment goals.

- Seek advice from SMSF professionals or financial advisers.

Setup Process:

- Register the SMSF with the ATO and open a fund bank account.

- Develop a compliant investment strategy.

Select Lender and Loan Type:

- Choose between bank or non-bank lenders based on your needs.

- Review and compare loan products with brokers.

Conduct Postcode Screening:

- Evaluate property location, growth potential, and rental demand.

Submit Documents for Audit and Tax Compliance:

- Ensure all required documents are ready for the annual tax filing.

7. FAQs

Q1: Can I set up an SMSF on my own?

A: While it is possible, SMSF setup can be complex, and it’s recommended to engage specialists to ensure compliance.

Q2: Are non-bank lenders reliable?

A: Yes, many non-bank lenders specialize in SMSF loans, offering more flexible terms and tailored products.

Q3: What do lenders consider for loan servicing?

A: They evaluate rental income, contributions, financial standing, LVR, and investment strategies.

Q4: Why is postcode screening important?

A: It helps identify properties with better growth potential, rental demand, and market stability.

Conclusion

By following the steps outlined in this guide and seeking expert advice, you can embark on your SMSF property investment journey with confidence. Careful planning, informed decision-making, and thorough research will ensure a smooth process, helping you maximize returns and secure your financial future.

ADDITIONAL RESOURCES:

ATO SMSF Property –https://www.ato.gov.au/individuals-and-families/super-for-individuals-and-families/self-managed-super-funds-smsf/smsf-newsroom/smsfs-investing-in-property

Contact Us – Contact Us – My SMSF (mysmsfproperty.com.au)