With the RBA continuing to keep interest rates at a high level, many homeowners are under stress. New data from realestate.com.au, accompanied by a finder survey, reveals that almost half of the mortgage holders are struggling to make their repayments. Due to these factors, property values might not be sustainable, and the possibility of a […]

With the RBA continuing to keep interest rates at a high level, many homeowners are under stress. New data from realestate.com.au, accompanied by a finder survey, reveals that almost half of the mortgage holders are struggling to make their repayments. Due to these factors, property values might not be sustainable, and the possibility of a market correction remains high. This is an economic environment filled with risks and opportunities for SMSF property investors.

Impact of Rising Rates on Property Markets and SMSF Investors

The RBA has been in an aggressive monetary policy tightening cycle since 2022 to control inflation. The cash rate has been increased from near-zero to 4.35%. The sharp rise in rates has driven up the borrowing costs of many Australians by thousands of dollars a year. Rental yields may no longer service loan repayments, particularly for SMSF trustees with LRBAs, placing pressure on fund cash flow.

Wage Growth Falling Behind Inflation

While the official RBA inflation rate has come down to 5%, Australians have been feeling a real level of inflation closer to 15% when housing, groceries, and fuel are taken into account. Continued low wage growth has taken purchasing power away from households in the wake of excessive inflation, compelling discretionary spending cuts.

This economic squeeze trickles down to SMSF property investors, as the increased cost of living eats away at the ability of tenants to pay higher rents and could force owners to dispose of properties, thereby adding to supply and driving prices lower still.

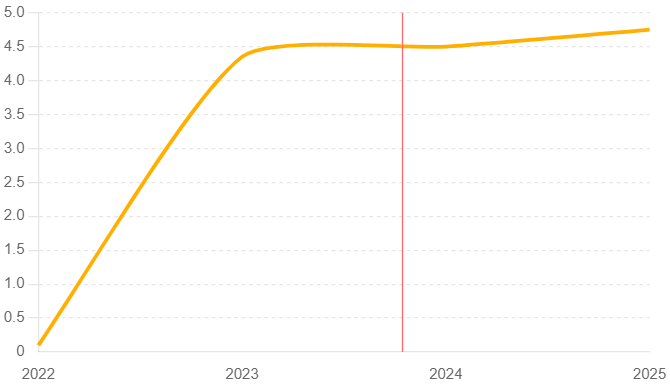

Interest Rate Trends (2022-2025)

| Year | Interest Rate (%) |

| 2022 | 0.10% |

| 2023 | 4.35% |

| 2024 | 4.50% (projected) |

| 2025 | 4.75% (projected) |

Market Correction and the Path Forward for SMSF Trustees

While a market correction is especially damaging to highly leveraged investors, it does ultimately provide opportunities for those who are prepared. Price declines-most significantly in Sydney and Melbourne-are predicted to continue through 2024-2025 as increased debt burdens outweigh wage growth and demand softens.

Property Price Projections (Sydney & Melbourne)

| Year | Sydney (AUD) | Melbourne (AUD) |

| 2022 | $1,200,000 | $1,100,000 |

| 2023 | $1,150,000 | $1,050,000 |

| 2024 | $1,050,000 | $980,000 |

| 2025 | $1,000,000 | $950,000 |

Key Strategies for SMSF Investors During Market Volatility

- Opportunities post-correction

Falling property prices can enhance rental yields, creating opportunities for SMSFs with liquidity or pre-approved loans to enter the market at favourable prices. - Reviewing Existing Loans

SMSFs holding LRBAs should carefully review loan terms and consider refinancing before lenders further tighten credit policies. Working with a specialised mortgage broker can help trustees access better loan conditions. - Diversifying Beyond Property

SMSFs should diversify their portfolios to manage risks in a high-rate environment. Allocating funds to fixed interest, shares, or uncorrelated market assets can provide stability amid property market volatility.

Risks for New Entrants and Highly Leveraged SMSFs

While a correction may offer better entry points, new entrants must do so with caution: if economic conditions deteriorate or unemployment rises, property yields could come under pressure, making it tough for SMSFs to service debt obligations from rental income alone.

There are also regulatory risks. For instance, the lenders’ constraints on SMSF borrowing can get even tighter. Access to credit will, therefore, be even more limited. For this reason, the trustees should devise a clear strategy regarding borrowing with respect to the long-range objectives of the fund to avoid these types of risks.

Conclusion: A Strategic Approach for SMSF Property Investors

The current environment of high inflation, wage stagnation, and increasing interest rates makes for a high level of proactivity required by SMSF trustees. Whether through refinancing, diversification of portfolios, or timing property acquisitions during a correction, a well-prepared SMSF should be able to navigate these challenges.

Key Takeaways:

- Monitor loan terms and refinance before lenders tighten policies further.

- Diversify into other asset classes to reduce exposure to property volatility.

- Ensure, new property purchases are timed for price corrections.

- Stay informed on economic trends and consult financial advisers regularly.

Stay abreast of economic trends, consulting financial advisers regularly.

While these latter types of growth strategies are significant for SMSF trustees, they need to make sure that prudent risk management is sought so as not to over-leverage and set themselves up for possible failure in the long term. With this said, your fund will be ready to capitalize on new opportunities while maintaining financial stability during these unsober times.