Contents Outline Introduction What Are SMSF Related Party Loans? Why Use SMSF Related Party Loans? How to Set Up an SMSF Related Party Loan Comparison: SMSF Related Party Loans vs Bank Loans ATO Guidelines on SMSF Related Party Loan Rates SMSF Loan Arbitrage Strategy Explained Conclusion FAQs Introduction – SMSF related party loans When […]

Contents Outline

Introduction – SMSF related party loans

When it comes to borrowing within an SMSF, trustees have two primary choices:

-

SMSF related party loans

-

Traditional bank-issued loans

While both options help fund property and other allowable SMSF investments, they differ in cost, approval process, and compliance requirements. Understanding SMSF related party loans, and the differences ensures your fund stays compliant with ATO SMSF loan rules.

What Are Related Party Loans?

An SMSF related party loan is when an SMSF borrows money from a related individual or entity, such as:

-

SMSF members,

-

Their relatives,

-

Companies or trusts controlled by the members.

Unlike bank loans, these are personal in nature but must still meet the ATO’s arm’s length requirements.

Benefits of Related Party Loans?

| Benefit | Explanation |

|---|---|

| ✅ Flexibility | Use funds for SMSF-compliant investments like property or shares. |

| ✅ Trust-Based Lending | Lower risk of loan default due to family relationships. |

| ✅ Potential Cost Savings | May offer lower fees than commercial banks. |

| ✅ Faster Approval | Fewer credit checks, less paperwork. |

⚠️ Important: All loan terms must be arm’s length to avoid breaching SMSF rules.

How to Set Up an SMSF Related Party Loan

Key Setup Steps:

| Step | Action |

|---|---|

| Draft a Loan Agreement | Include loan amount, interest rate, repayment terms. |

| Set Arm’s-Length Interest Rates | Must reflect commercial market rates. |

| Establish Repayment Terms | Regular repayments aligning with market practices. |

| Document Every Transaction | Keep clear records for audits. |

| Check Tax and Legal Implications | Ensure compliance with ATO guidelines. |

| Review Periodically | Adjust terms if regulations change. |

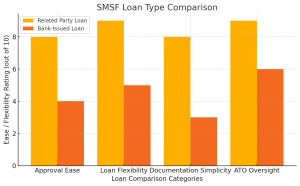

Comparison: SMSF Related Party Loans vs Bank Loans

| Feature | SMSF Related Party Loans | Bank-Issued Loans |

|---|---|---|

| Interest Rate (2024/25) | 9.35% (arm’s length) | Variable, based on credit score |

| Approval Process | Flexible, trust-based | Strict, based on financial assessment |

| Documentation | Loan agreement + minimal paperwork | Full financial verification |

| ATO Oversight | High – Must meet arm’s length rules | Moderate – Standard banking compliance |

| Loan Flexibility | High | Limited to bank policies |

ATO Guidelines on SMSF Related Party Loan Rates

The ATO requires related party loans to mirror market terms. This means the interest charged cannot be lower or higher than what a bank would offer.

👉 Example Interest Rate (2024–25 for Real Property Loans):

| Year | Minimum Arm’s Length Rate |

|---|---|

| 2024–2025 | 9.35% |

📄 Reference: ATO Safe Harbour Guidelines

SMSF Loan Arbitrage Strategy Explained

How Arbitrage Works:

-

An individual borrows from a bank at a lower retail rate (e.g., 6%).

-

They lend to their SMSF at the ATO-approved rate (e.g., 8.85%).

-

The interest margin (~2.85%) is profit.

That profit can be:

-

Contributed back into the SMSF (subject to contribution caps).

-

Used to grow the SMSF balance.

⚠️ Contributions must comply with ATO contribution limits.

Conclusion

SMSF related party loans offer a flexible and potentially cheaper way to finance superannuation investments, compared to bank loans. However, strict ATO rules ensure these loans are not misused.

✔️ Always seek legal and financial advice before arranging a related party loan.

Frequently Asked Questions

❓ Can my SMSF borrow from a family member?

Yes, but the loan terms must be commercial, and interest rates should match market rates.

❓ What happens if I charge a lower interest rate than the ATO guidelines?

The ATO may treat the loan as a non-compliant arrangement, leading to tax penalties.

❓ Are bank loans easier than related party loans?

Banks have stricter approval processes but less regulatory scrutiny post-setup.

Additional Resources:

- ATO Safe Harbour Rates – Related Party Loans

- My SMSF Loans– Types of SMSF loans

General Advice Warning:

This article contains general information only. It does not consider your personal objectives, financial situation, or needs. Before acting on this information, you should seek professional financial, tax, and legal advice to assess whether it is appropriate for your circumstances.