SMSF Property vs Bank of Mum and Dad Contents Introduction Key Statistics: Bank of Mum and Dad What Is SMSF Property? Strategy 1: Using SMSF to Enter the Property Market Why This Strategy Works The Long-Term Trade-Off Strategy 2A: Selling SMSF Property to Eliminate Debt Strategy 2B: Keeping SMSF Property for Retirement Income Example Scenarios […]

SMSF Property vs Bank of Mum and Dad

Contents

In Australia, the “Bank of Mum and Dad” has become a critical financial resource, helping younger generations enter the property market. With rising housing costs and tighter lending criteria, parents frequently assist their children by gifting deposits, providing loans, or acting as guarantors.

Key Facts and Figures: Bank of Mum and Dad (Australia)

- Fifth-largest lender in Australia as of 2023.

- Contributed over $35 billion towards property purchases since 2021.

- Average assistance amount: $89,000 per child.

- Approximately 60% of first-home buyers rely on parental financial support (Source: Digital Finance Analytics, 2023).

| Year | Total Contributions ($ Billion) | Average Gift Size ($AUD) |

| 2021 | $24 | $83,000 |

| 2022 | $31 | $87,000 |

| 2023 | $35 | $89,000 |

SMSF Property: An Alternative Solution

An SMSF (Self-Managed Super Fund) property investment offers a unique way to enter the property market without placing financial strain on parents or compromising personal cash flow. However, properties within an SMSF cannot be personally accessed or lived in until retirement (age 60).

Strategy 1: Entering the Market Without Cash Flow Strain

SMSF property allows younger Australians to invest in real estate using their accumulated super savings rather than personal funds, significantly reducing financial strain and lifestyle impact. This may work well, where it is a pooled SMSF where all members; noting SMSF may have up to six members; who receive employer super contributions may use contributions, rental income and other income to repay the SMSF loan faster.

SMSF Income Streams:

- Rental income

- Super contributions

- Interest and PAYG variations

Note: all taxed at 15% compared to the average tax rate of 37% for property held outside superannuation

Why This Strategy Works:

- Super Contributions Fund Investments: Employer super contributions (SG), rental income, and salary-sacrificed amounts fund loan repayments.

- Preserves Personal Borrowing Capacity: Does not affect personal mortgage or borrowing limits.

- Capital Growth: Enables asset growth, safeguarding against future market price increases.

The Long-Term Trade-Off:

- Property can only be accessed or lived in upon retirement (typically at age 60).

Strategy 2: SMSF Property as Retirement Income or Debt Elimination

Option A: Selling SMSF Property to Pay Off Home Debt

Holding property in an SMSF becomes particularly powerful as capital gains become tax-free upon entering the pension phase at age 60.

How It Works:

- Property Purchased Within SMSF: Using super contributions and rental income.

- Asset Growth: The property appreciates over decades.

- Tax-Free Sale in Pension Phase: Selling the property after retirement incurs no capital gains tax.

- Clear Personal Mortgage: Proceeds can fully eliminate personal home debt.

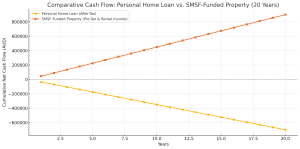

Example Scenario:

| Description | Amount ($AUD) |

| Initial SMSF Property Cost | $600,000 |

| Value at Retirement (Age 60) | $1,200,000 |

| Capital Gains Tax | $0 (Tax-Free) |

| Proceeds for Personal Debt | $1,200,000 |

Assumptions: Couple are aged 40 and retire at 60

Option B: Keeping SMSF Property for Tax-Free Rental Income

Instead of selling, retirees can keep the SMSF property and enjoy ongoing rental income.

How It Works:

- At retirement, switch SMSF to pension phase.

- Rental income becomes tax-free, providing continuous retirement income.

Example Scenario:

| Annual Rental Income | Tax During Pension Phase |

| $50,000 | $0 (Tax-Free) |

Final Thoughts: A Strategic Alternative

Educating younger Australians and their families about SMSF property investing offers a robust alternative to the traditional “Bank of Mum and Dad”. It facilitates property ownership without straining parents’ financial resources and helps secure a comfortable retirement.

Conclusion:

While restricted by delayed access (until age 60), SMSF property investments offer compelling long-term benefits, positioning Australians strategically for financial security and reduced dependency on family resources. Always seek financial and tax advice in relation to SMSF property strategies.

FAQs

1. Can my SMSF help my children buy a home directly?

No. SMSFs cannot provide financial assistance to family members. However, SMSFs can invest in property for the fund’s benefit, not for personal use or gifting.

2. Can I live in my SMSF property before retirement?

No. SMSF-owned properties are strictly for investment purposes and cannot be lived in by members or related parties before retirement.

3. When can I sell an SMSF property and access the money?

You can sell the property once you reach preservation age and meet a condition of release (e.g. retirement). In the pension phase, capital gains on sale may be tax-free.

4. What happens to the SMSF property when I retire?

You can either sell the property to fund your pension (tax-free) or retain it and receive rental income tax-free as long as the SMSF is in pension phase.

5. Can my SMSF property help me pay off my home loan?

Yes—indirectly. Upon retirement, you can sell the SMSF property and withdraw a tax-free lump sum, which you can use to pay off personal debts like your home loan.

Additional Resources

General Information Warning: This article represents information intended for educational purposes only. It is not specific to anyone’s circumstances, rendering it general. Please seek financial advice relative to your personal financial situation.