Strategic Liquidity Management in SMSFs — Why It Matters More Than Ever Contents Introduction Understanding Liquidity in SMSFs Why Liquidity Risk Has Risen The Regulatory View — ATO and SIS Act Expectations Developing a Liquidity Strategy Case Study — Property and Pension Payments Practical Risk Management Tools FAQs External Resources Disclaimer Introduction In recent years, […]

Strategic Liquidity Management in SMSFs — Why It Matters More Than Ever

Contents

Introduction

In recent years, the focus for many Self-Managed Super Fund (SMSF) trustees has been on performance property growth, crypto diversification, and tax efficiency. Yet, one of the most overlooked risks in SMSFs is liquidity.

When markets tighten, pension payments fall due, or unexpected expenses arise, an illiquid SMSF can quickly breach compliance obligations or force asset sales at the wrong time.

This article explores how trustees can design a liquidity strategy, in line with SIS Regulation 4.09, to protect both member benefits and compliance integrity.

Understanding Liquidity in SMSFs

Liquidity refers to how easily an SMSF’s assets can be converted to cash to meet obligations such as:

-

Minimum pension payments (Reg. 1.06(9A))

-

Tax liabilities (e.g., CGT on disposals)

-

Life insurance premiums

-

Audit and administration fees

An SMSF with heavy exposure to direct property or collectibles can be “asset rich, cash poor,” making it vulnerable to breaches of the sole purpose test and member payment delays.

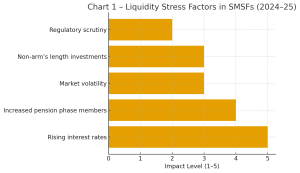

Why Liquidity Risk Has Risen

| Risk Driver | Impact on Liquidity | Notes |

|---|---|---|

| Rising interest rates | Higher loan repayments reduce free cash | Particularly in LRBA property funds |

| Increased pension phase members | More cash outflow due to minimum drawdowns | Liquidity pressure increases with ageing members |

| Market volatility | Difficulties liquidating crypto or shares quickly | Bid–ask spreads widen in downturns |

| Non-arm’s length investments | Restrictions on redemption or sale | ATO scrutiny on related-party loans |

| Regulatory stress testing | Auditors and ATO reviewing liquidity planning | Documentation required under Reg. 4.09 |

Visualising the problem:

The Regulatory View — ATO and SIS Act Expectations

Key Regulatory Points:

-

SIS Regulation 4.09 requires trustees to formulate and give effect to an investment strategy that considers liquidity.

-

The ATO’s SMSFR 2008/1 ruling further requires trustees to review that strategy regularly and ensure sufficient liquidity for benefit payments.

-

Auditors must check whether the fund’s liquidity strategy is reasonable, documented, and reviewed annually.

In 2023, the ATO issued compliance reminders noting that liquidity failures were a key contributor to SMSF wind-ups and contraventions reported under Auditor Contravention Reports (ACRs).

Developing a Liquidity Strategy

1. Set a Target Liquidity Ratio

Maintain a minimum cash-to-asset ratio of 5–10% (more for pension-heavy funds).

Use this as a dynamic benchmark, adjusting after large acquisitions or withdrawals.

2. Align Pension Timing with Cash Inflows

Synchronise rental or dividend income schedules with pension payments.

Consider quarterly or semi-annual cash-flow projections.

3. Stress Test the Portfolio

Model adverse scenarios:

-

10% market fall

-

One property vacancy for six months

-

Emergency expenses of $15,000

This helps trustees quantify real-world liquidity gaps.

4. Build a Contingency Plan

Maintain readily realisable assets, such as ETFs or term deposits, to cover short-term needs.

Document fallback options (e.g., temporary suspension of contributions, sale sequencing order).

Case Study — Property and Pension Payments

| Scenario | Details |

|---|---|

| Fund assets | $1.2M total: $900K property (LRBA), $150K shares, $150K cash |

| Members | Two in pension phase (65 & 68) |

| Annual pension drawdown | $60,000 |

| Loan repayments | $40,000 p.a. |

| Liquidity coverage | Cash covers ~1.5 years of obligations |

If one tenant defaults or property repairs arise, the fund could face a shortfall.

Mitigation:

-

Rebalance 10% from shares into cash/term deposits

-

Review rental yield projections

-

Document this action in trustee minutes and investment strategy review

Practical Risk Management Tools

| Tool | Purpose | Best Use Case |

|---|---|---|

| Cash flow projection spreadsheet | Quantifies upcoming obligations | Annual planning and audits |

| Stress-testing model | Simulates liquidity shocks | When adding large illiquid assets |

| SMSF Investment Strategy Review | Ensures compliance under Reg. 4.09 | Annual review |

| Segregated asset pools | Protects liquidity for pension phase | Multi-member funds |

| Liquidity coverage ratio | Tracks monthly liquidity percentage | Ongoing monitoring |

FAQs

1. How often should I review liquidity in my SMSF?

At least annually, or whenever a major asset is bought/sold or a member moves into pension phase.

2. What happens if I can’t meet my pension payments?

You may breach pension standards and lose ECPI (Exempt Current Pension Income) status — meaning your fund pays tax on what would otherwise be exempt income.

3. Does crypto affect liquidity risk?

Yes. Crypto assets can be highly volatile and illiquid under stress — they should be capped within your risk tolerance (typically ≤10% for diversified funds).

4. Are term deposits sufficient for liquidity coverage?

Yes, provided they mature within 12 months and match your cash-flow requirements.

External Resources

-

ATO – Investment Strategy Requirements – click here

-

SIS Regulation 4.09 (AustLII) – click here

-

My SMSF Contact Us – click here

-

ASIC – Self-Managed Super Fund Risks – click here

Disclaimer

This article provides general information only and does not constitute personal financial advice. Trustees should seek professional guidance tailored to their fund’s investment objectives, member circumstances, and liquidity needs.