Proposed Tax Law Changes in Australia (2026): What They Mean for SMSFs and Property Investors Contents The Policy Shift: What Is Actually Changing Capital Gains Tax (CGT) Reform Negative Gearing Reform Superannuation Changes (Division 296) Impact on SMSFs Impact on Property Investors Strategic Considerations Key Risks and Opportunities FAQs General Advice Warning The Policy Shift: […]

Proposed Tax Law Changes in Australia (2026): What They Mean for SMSFs and Property Investors

Contents

-

The Policy Shift: What Is Actually Changing

-

Capital Gains Tax (CGT) Reform

-

Negative Gearing Reform

-

Superannuation Changes (Division 296)

-

Impact on SMSFs

-

Impact on Property Investors

-

Strategic Considerations

-

Key Risks and Opportunities

-

FAQs

-

General Advice Warning

The Policy Shift: What Is Actually Changing

Australia is entering a structural tax reform cycle, not simply a minor adjustment phase. The Federal Government’s direction is clear, and practitioners should treat these proposals as a genuine reorientation of tax policy rather than routine tinkering.

Three themes dominate the reform agenda: scaling back tax incentives for property investors, increasing taxation on large superannuation balances, and rebalancing the treatment of wealth relative to income. Together, these changes represent the most significant overhaul of investment taxation in a generation.

The government’s stated rationale centres on reducing tax advantages tied to capital growth assets, improving intergenerational equity, and redirecting revenue toward broader reform. Understanding the intent behind each measure helps in anticipating how rules will evolve, and where to position before the settings change.

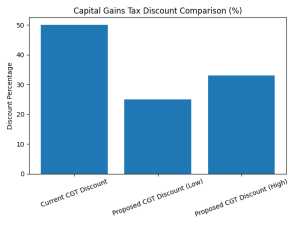

Capital Gains Tax (CGT) Reform

The Current System

Currently, taxpayers who hold an asset for more than 12 months receive a 50% discount on any capital gain. This concession has been central to property and equity investment strategy for decades, effectively halving the effective tax rate on long-term capital growth.

What the Government Proposes

Proposed changes would either reduce the discount to between 25% and 33%, or replace the discount model entirely with inflation indexation meaning only the real, inflation-adjusted gain would attract tax. The government has not yet settled on a final model, and strong indications suggest a hybrid approach may emerge.

Grandfathering and Transitional Treatment

There is considerable expectation that existing assets will receive some degree of grandfathering,that is, the current 50% discount would continue to apply to gains accrued before the change takes effect. However, grandfathering is not guaranteed, and practitioners should not rely on it without legislative confirmation. A hybrid model, applying different treatment to pre- and post-reform gains, remains a live possibility.

Why This Reform Matters

The current CGT discount rewards long-term capital appreciation and reinforces leveraged property investing as a primary wealth-building strategy. Reform would directly reduce after-tax returns on property and growth assets, and consequently lower the attractiveness of buy-hold-sell strategies that have defined Australian investor behaviour for decades. In short, the economics of holding appreciating assets become measurably less compelling under any of the proposed models.

Negative Gearing Reform

How the Current System Works

Under the current rules, investors can offset property losses,where interest and holding costs exceed rental income,against their personal income. This deduction reduces taxable income and effectively transfers part of the cost of holding loss-making property to the public revenue base. Combined with the CGT discount, negative gearing forms the core engine of leveraged property investment in Australia.

The Options Under Consideration

The government is considering several approaches. These include full removal of negative gearing for new investments, a cap restricting deductions to one or two properties, limiting negative gearing to new housing only, or removing access entirely for high-volume investors. Each option carries different implications for existing and prospective investors.

The Practical Impact

Reforming negative gearing reduces investor demand, targets high-income earners who derive the greatest benefit from the current concession, and shifts incentives toward owner-occupiers. In the short term, the revenue impact is modest; however, over the long term the fiscal and behavioural consequences are significant. Furthermore, removing negative gearing in combination with a reduced CGT discount amplifies the impact on leveraged property strategies beyond what either reform achieves independently.

Superannuation Changes (Division 296)

The Division 296 changes are separate from the CGT and negative gearing reforms but are equally material for clients with larger super balances. The government has confirmed that superannuation balances above $3 million will attract an additional tax, lifting the effective rate to up to 30% on earnings attributable to the excess balance. This measure applies from 1 July 2026.

The broader implication is a structural shift in how policymakers position superannuation. Super is moving away from functioning as a broadly accessible tax-advantaged wealth accumulation vehicle, and toward a more narrowly targeted retirement savings system. For trustees and members with balances approaching or exceeding the $3 million threshold, this changes both the accumulation and drawdown calculus considerably. Advisers should factor this shift into long-term structural recommendations rather than treating it as a one-off adjustment.

Impact on SMSFs

Property Inside SMSFs Becomes Less Tax-Efficient

The proposed CGT changes directly affect SMSFs that hold real property as a core asset. CGT concessions available to SMSFs may reduce under the reform models, and exit strategies,particularly the sale of property approaching or during pension phase, become less efficient from a tax perspective. Trustees who have relied on the fund’s low tax environment to maximise property returns will need to reassess their projections.

Liquidity Pressure for Large and Property-Heavy Funds

Division 296 introduces liquidity risk for SMSFs with balances above $3 million, particularly those heavily invested in illiquid assets such as direct property. Property cannot be partially sold to meet a tax liability, and the fund may not hold sufficient liquid assets to pay the additional tax without a forced sale or the member making a personal contribution to cover the shortfall. This risk is especially pronounced in single-asset or dual-asset funds where property represents the overwhelming majority of the portfolio.

Strategy Shift: From Property-Driven to Income-Focused

As a result of these pressures, many SMSFs will need to pivot their investment strategy toward income-producing assets rather than capital-growth-focused ones. In practice, this means greater diversification beyond direct property, with increased allocation to listed equities, private credit, and alternative income-generating assets. Exit strategy,previously a secondary consideration,becomes a first-class planning decision in this environment.

Structural and Legislative Risk

SMSFs with heavy exposure to residential property or single-asset strategies now carry a form of risk that is distinct from market risk: legislative risk. Policy concentration in a single asset class that is a direct target of reform amplifies the consequences of rule changes. This warrants a frank review of concentration positions and a clear-eyed assessment of whether current structures remain fit for purpose.

Impact on Property Investors

Reduced After-Tax Returns

The combined effect of CGT and negative gearing reform materially reduces after-tax returns on leveraged property strategies. The table below summarises the key components under current and proposed settings.

The net result is a lower internal rate of return on leveraged property strategies. Investors who have modelled returns on the basis of current concessions will need to revise their assumptions materially.

Investor Demand Is Already Responding

Evidence already suggests that investors are pausing new purchases in anticipation of reform. This behavioural shift,even before legislation passes,reflects the sensitivity of leveraged property strategies to changes in the tax settings that support them. As demand from investors eases, the dynamics of the purchase market shift toward owner-occupiers.

Rental Market Consequences

Reduced investor demand is likely to constrain new rental supply over the medium term. However, analysts expect any resulting rent increases to be modest rather than extreme, given that supply constraints are structural rather than driven solely by investor behaviour. That said, the rental market impact warrants monitoring, particularly in markets where investor-owned stock represents a large share of the rental pool.

Shifting Asset Preferences Among Investors

Investors facing less favourable treatment of property are likely to hold existing assets longer,particularly where grandfathering applies, and redirect new capital toward shares, trust structures, and alternative investments. This represents a broader reallocation away from leveraged property as the default wealth-building vehicle. In practice, advisers should expect increased interest in restructuring and diversification conversations over the coming months.

Strategic Considerations

Timing Becomes a Critical Variable

Pre-reform acquisitions may retain existing concessions, making the timing of new investments and disposals a significant planning lever. Post-reform assets will attract lower tax efficiency under any of the proposed models. Consequently, clients who are considering property purchases or SMSF asset changes should understand how their timing interacts with any grandfathering provisions.

Structure Now Drives Outcomes

As the tax efficiency of direct property holding declines, structure becomes a more important differentiator. Advisers should expect increased use of trusts, corporate structures, and diversified SMSF strategies as clients seek to optimise their position within the new settings. In particular, clients currently holding property in their own name,rather than through a structure, face the starkest reassessment.

Exit Strategy Is Now a First-Class Decision

Previously, investment strategy centred on the entry decision: which asset, at what price, with what financing. Under the reformed settings, exit tax outcomes may define overall investment success as much as entry does. Advisers should incorporate exit modelling into every property and SMSF strategy review, rather than treating disposal as a decision for the future.

Key Risks and Opportunities

Risks

Policy uncertainty remains the dominant risk. The rules are still evolving, and final legislation may differ from current proposals in ways that affect planning already underway.

Reduced tax arbitrage means the gap between property investment returns and alternative asset classes narrows. Strategies that depended on tax concessions to generate acceptable after-tax returns will underperform expectations.

Overexposure to property in SMSFs creates both legislative and liquidity risk, particularly for funds approaching or exceeding the Division 296 threshold.

Liquidity constraints are a practical concern for property-heavy funds facing new tax obligations without liquid assets to meet them.

Opportunities

Early positioning before Parliament legislates reforms allows clients to restructure or acquire assets under existing concessions where appropriate.

Asset diversification becomes both a risk-management imperative and a genuine opportunity to broaden return sources beyond a single asset class.

Income-focused strategies are likely to attract stronger relative returns in a post-reform environment, as the CGT discount that currently favours capital growth winds back.

Reduced competition from leveraged investors may create entry opportunities in some asset classes for those with structures already optimised for the new environment.

FAQs

Will existing properties be affected?

Existing properties are likely to receive partial protection through grandfathering provisions, but this is not legislatively guaranteed. In practice, grandfathering may apply to gains accrued prior to the reform date, while gains accrued afterward attract the new, lower discount or indexation model. Clients should not make irreversible decisions on the assumption of full grandfathering until legislation confirms the scope of any transitional relief.

Will house prices fall?

A modest price impact is the broadly expected outcome, but the supply-demand balance remains the dominant price driver — not tax concessions alone. Reduced investor demand will apply downward pressure at the margin, particularly in higher-price markets where negatively geared investors are more concentrated. However, structural undersupply continues to provide a floor for prices in most major Australian markets.

Are SMSFs still viable for property investment?

Yes, SMSFs remain viable vehicles for property, but the underlying logic shifts from tax-driven to strategy-driven. In the current environment, the tax concessions available inside super made property attractive even where the commercial case was marginal. Under the proposed reforms, property in an SMSF needs to stand up on its own investment merits — yield, liquidity, and portfolio fit — rather than relying primarily on concessional tax treatment.

Should investors act now?

This depends on each client’s time horizon, structural position, and level of exposure to the proposed changes. For clients with large property holdings inside super, near-term liquidity planning is prudent regardless of whether reforms pass in their current form. For clients considering new acquisitions, a careful comparison of pre- and post-reform returns — across different asset structures — warrants attention before committing capital.

Useful Links

1. ABC News – Click here

2. Contact My SMSF for new SMSFs and SMSF Transfers – Click here

General Advice Warning

The information contained in this article is general in nature and does not constitute financial product advice, tax advice, or legal advice. It does not take into account your personal objectives, financial situation, or needs. The proposed legislative changes discussed in this article are subject to parliamentary process and may be amended, deferred, or not enacted in their current form. Before acting on any information in this article, seek independent advice from a qualified financial adviser, tax adviser, or legal practitioner who can assess the relevance of this information to your specific circumstances.