Rising costs of retirement — why lifestyle essentials are squeezing retirees and what to do about it The latest ASFA Retirement Standard confirms the uncomfortable reality, which is that the essentials, food, private health insurance and electricity are driving the rise in the cost of a comfortable retirement. For a 65-year old couple, ASFA now […]

Rising costs of retirement — why lifestyle essentials are squeezing retirees and what to do about it

The latest ASFA Retirement Standard confirms the uncomfortable reality, which is that the essentials, food, private health insurance and electricity are driving the rise in the cost of a comfortable retirement. For a 65-year old couple, ASFA now estimates an annual comfortable budget of A$75,319; for a single, A$53,289. These figures are updated quarterly and reflect real consumer-price pressures on the items retirees rely on most.

Contents

- Quick summary and why it matters

- What’s changed — the essentials driving the increase

- Why retirees are vulnerable now

- Three focus areas trustees and advisers must prioritise

- Investment performance (with a plan)

- Fee transparency

- Tax efficiency

- Practical checklist — immediate actions trustees and advisers can take

- Illustrative stress-test (table + chart)

- FAQs

- Disclaimer

Quick summary

These essential household items are rising faster than many other items. The ASFA figures show that private health insurance, electricity and fresh food are the main contributors to the quarter-on-quarter increase in the “comfortable” retirement standard. This squeezes fixed retiree budgets and elevates the importance of investment consistency, fee discipline and tax-aware withdrawal planning.

What’s changed — the essentials driving the increase

Over the last twelve (12) months, ASFA flagged meaningful price rises in three categories that hit retirees disproportionately:

- Private health insurance — premiums have increased materially (out-of-pocket costs are compounding pressure on budgets).

- Household utilities (electricity) — energy price volatility and policy-driven adjustments have pushed bills higher.

- Grocery bills (fresh food) — supply chain and weather-driven pressures are elevating food costs.

Those line items alone explain a material portion of the rise in ASFA’s comfortable-standard figures.

Why this matters now

Retirees typically live off fixed assets like property or dividend income and term deposit interest which are typical steady income streams for SMSF retirees across Australia. However, when necessity costs rise faster due to real world inflation pressures and higher than typical investment returns, we get increases lifestyle cost pressures that can hasten the erosion of retirement asset capital values:

- discretionary spending quickly disappears.

- those holding illiquid assets (property, farms, private businesses) may face cash-flow strain; and

- trustees must reconcile income-matching objectives with concentrated inflation risks to stay ahead

Even modest, repeated quarterly rises amplify into meaningful dollar shortfalls over a decade and this is the why a passive approach is insufficient. Pre-retirees and retirees must take action now.

Three focus areas trustees and advisers should prioritise

- Investment performance, but with a plan

Headline returns are attractive, but retirees need predictable, liquid income. Practical considerations:

- Favour higher-quality income sources (franked equities, listed infrastructure, investment-grade credit) for the portion of the portfolio paying day-to-day expenses;

- maintain a growth insulation for long-term purchasing-power protection, but avoid forcing sales of illiquid holdings; and

- stress-test portfolios for inflation concentrated in essentials (not just headline CPI). Run scenarios that lift health, energy and food costs ahead of general inflation.

- Fee transparency — every basis point counts

Fees compound and reduce sustainable withdrawal rates. Trustees should:

- demand itemised fee disclosure (administration, platform, underlying management fees, transaction fees);

- translate fee drag into dollars for members (e.g., “0.50% = $X p.a.”); and

- prefer low-cost core ETFs where appropriate; use active managers only where repeatable, after-fee alpha is demonstrable.

- Tax efficiency — retain more of what you earn

Tax settings materially affect net retirement income. Actions include:

- sequencing drawdowns (income vs capital) to minimise tax leakage;

- checking concessional and non-concessional cap usage; and

- for SMSFs, keeping meticulous records to substantiate tax positions and to prepare for potential legislative change.

Practical checklist — quick actions to start today

- Re-run cash-flow stress tests, modelling +5% / +10% / +15% increases in health, electricity and grocery budgets.

- Request a fee-breakdown from your platform and from your adviser so that they can produce a one-page “what you pay” for each member (in dollars).

- Review liquidity: ensure the fund can meet a 12-month spike in essential cost increases without forced asset sales. If not, plan partial sales or income overlays with documented governance.

- For SMSFs: update trustee minutes recording the rationale for any allocation or liquidity changes. Remember auditors and the ATO expect governance.

- Communicate: send members a plain-English note explaining the pressures and the fund’s response. Transparency reduces panic and preserves trust.

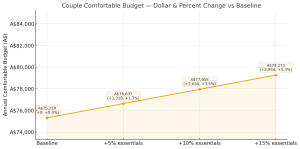

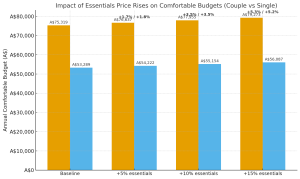

Illustrative stress-test

Below is an illustrative stress test showing how modest rises in essentials costs could affect ASFA’s comfortable-standard budgets.

Assumption (illustrative): essentials (health, electricity, food) represent 35% of the comfortable budget. The table shows baseline budgets (ASFA) and the effect of a +5% / +10% / +15% increase in those essentials.

The interactive table (displayed for you) summarises the outcomes; key lines:

- Baseline (ASFA): Couple A$75,319 — Single A$53,289.

- With a 10% increase in essentials (illustrative), a couple’s comfortable budget rises to A$77,769 — an increase of A$2,450 p.a.; a single’s budget rises by A$1,734 p.a.

(The detailed table and chart are illustrative stress tests using the assumptions stated; they are not ASFA releases, but a model to show sensitivity.)

FAQs

Q1: Is ASFA’s figure my guarantee of cost?

No. ASFA’s figures are benchmarks for a “comfortable” retirement. Your cost depends on location, health, lifestyle and housing. Use ASFA as a guide and run personalised cash-flow modelling.

Q2: Will the government step in to help with rising costs?

Social policy is always possible, but retirees should not rely on ad hoc government measures. Plan using conservative scenarios and documented governance.

Q3: Should SMSFs sell property to cover increased living costs?

Not automatically. Property is illiquid and taxed differently. Consider staged sales, reverse mortgages (with caution), or income overlays — always document trustee decisions.

Q4: How often should I update my fund’s stress tests?

At least annually, and after any significant market move or policy change (e.g., tax reform, SG changes). Also run “what-if” scenarios quarterly for inflation spikes.

Q5: How can advisers show fee drag to members?

Calculate fee drag in dollar terms for each member (example: a 0.50% extra fee on A$500,000 = A$2,500 p.a.). Show the cumulative cost over 5–10 years to make the impact tangible.

| Scenario | Couple budget (A$) | Increase vs baseline (A$) | Single budget (A$) | Increase vs baseline (A$) |

| Baseline | 75,319.00 | 0.00 | 53,289.00 | 0.00 |

| +5% essentials | 76,635.58 | 1,316.58 | 54,217.22 | 928.22 |

| +10% essentials | 77,952.16 | 2,633.16 | 55,145.44 | 1,856.44 |

| +15% essentials | 79,268.74 | 3,949.74 | 56,073.66 | 2,784.66 |

(These stress scenarios are illustrative only. They use 35% essentials share assumption and are intended to show sensitivity, not to replace personalised advice.)

Disclaimer

This article is general information only and is not financial, tax, legal or investment advice. The ASFA figures quoted are used as published benchmarks; the stress-test scenarios in this article are illustrative and use stated assumptions (not ASFA-provided breakdowns). You should seek personalised financial and tax advice before making decisions based on this content. My SMSF / My SMSF Property accepts no liability for losses arising from reliance on this article.