SMSF Audit Contraventions and What You Can Do Every SMSF must undergo an annual audit to remain compliant. If your auditor finds a breach of the Superannuation Industry (Supervision) Act 1993 (SISA) or related regulations, it may be reported to the ATO in an Auditor Contravention Report (ACR). These reports can trigger serious consequences unless […]

SMSF Audit Contraventions and What You Can Do

Every SMSF must undergo an annual audit to remain compliant. If your auditor finds a breach of the Superannuation Industry (Supervision) Act 1993 (SISA) or related regulations, it may be reported to the ATO in an Auditor Contravention Report (ACR). These reports can trigger serious consequences unless promptly addressed.

This article breaks down:

-

The most common audit contraventions,

-

How to fix them,

-

What you may pay for rectification,

-

And how to protect your fund from being made non-compliant.

Table of Contents

Top 3 Most Common Contraventions

| Contravention | Description |

|---|---|

| Loans to Members | Lending SMSF money to a member or relative is illegal under SISA section 65. This is considered illegal early access. |

| In-House Asset Rule Breaches | More than 5% of fund assets invested in related entities breaches sections 82–85. Often caused by loans to related businesses or property. |

| Separation of Assets | Assets not held in the SMSF’s legal name (e.g. property titled in a trustee’s personal name). This violates the separation requirement. |

Remedial Steps for Trustees

To address an ACR or breach:

| Step | Action |

|---|---|

| 1. Understand the Breach | Review the auditor’s report and management letter. Confirm the SISA section breached and circumstances. |

| 2. Rectify Promptly | Repay illegal loans, sell excess in-house assets, or retitle SMSF assets correctly. |

| 3. Consider Voluntary Disclosure | Use the ATO’s SMSF Early Engagement and Voluntary Disclosure service. Fixing issues early can lead to penalty reductions. |

| 4. Keep Evidence | Save bank statements, trustee minutes, legal documents and updated asset records. |

| 5. Cooperate with the ATO | Be responsive if contacted. Show you understand the breach and have rectified it. |

Consequences of Non-Rectification

| Consequence | Impact |

|---|---|

| Fund Made Non-Compliant | Loss of 15% concessional tax rate; income taxed at 45%. Past income may be reassessed and taxed. |

| Administrative Penalties | Fines up to $16,500 per trustee per breach (based on 60 penalty units at $275 each in 2025). |

| Civil/Criminal Action | For severe breaches, the ATO may seek court penalties, disqualification as trustee, or criminal prosecution. |

MySMSF Auditor Fee Guide

Please refer to the interactive table above for a breakdown of MySMSF’s fees by severity level. Here’s a quick summary:

-

Low-Level Breach: $220 – $500

-

Moderate Breach: $500 – $1,200

-

Complex/Multiple Breaches: $1,200 – $2,200

These fees include liaising with trustees, revising financials, preparing rectification documents, and managing voluntary disclosure with the ATO and Auditor fees.

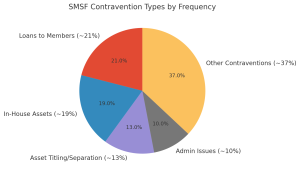

Contravention Frequency Breakdown

Below is a pie chart representing the frequency of different types of SMSF contraventions based on ATO audit statistics.

Key Insight: Over 50% of SMSF audit issues stem from just three ( 3) breaches: 1. loans to members, 2.in-house asset excesses, and 3.asset titling issues.

Practical Action Plan for Trustees

| Step | Action |

|---|---|

| 1. Review the Audit Report | Understand the nature and scope of the breach. |

| 2. Talk to the Auditor | Clarify the issue, timeline, and rectification expectations. |

| 3. Rectify | Pay back loans, dispose of assets, correct titles, and document everything. |

| 4. Disclose to ATO | Proactively use the ATO’s disclosure service to show good faith. |

| 5. Strengthen Compliance | Update your investment strategy, educate trustees, and consider engaging an SMSF administrator. |

smsf-audit-contraventions – understanding auditors jargon

FAQs

1. Do I have to disclose a contravention to the ATO?

No, the auditor will do this via a ACR( Audit Contravention Report), voluntary disclosure is strongly recommended. It can significantly reduce penalties.

2. Can SMSF assets be used to pay ATO fines?

No. Administrative penalties must be paid personally by the trustee. SMSF funds cannot be used for these payments.

3. How can I prevent future contraventions?

Stay educated, review your investment strategy regularly, keep clean records, and engage an experienced SMSF accountant or administrator.

Additional Resources

Disclaimer

The information provided in this article is general in nature and does not take into account your specific financial circumstances. You should seek independent legal, tax, or financial advice tailored to your situation before taking action. MySMSF and its representatives do not accept liability for any loss arising from reliance on this article.