Do SMSFs Need to Pay Land Tax? An Updated 2025–26 Guide for Trustees 📘 Contents Overview: What is Land Tax? How Land Tax Applies to SMSFs 2025–26 Land Tax Rates by State and Territory (SMSF Thresholds) Strategies to Reduce SMSF Land Tax Frequently Asked Questions Conclusion Disclaimer Useful Links Overview: What is Land Tax? Land […]

Do SMSFs Need to Pay Land Tax?

An Updated 2025–26 Guide for Trustees

📘 Contents

Overview: What is Land Tax?

Land tax is a state-based tax applied annually to the unimproved value of land owned by individuals, companies, and trusts including Self-Managed Super Funds (SMSFs).

Each state and territory has unique rules regarding:

-

Thresholds – the minimum land value before tax applies

-

Rates – the percentage charged on value above the threshold

-

Exemptions – principal residence, primary production land, and more

For SMSFs, land tax is a recurring compliance cost that must be accounted for when investing in property.

How Land Tax Applies to SMSFs

1. Direct Ownership

When your SMSF owns a property in its own name, it will be taxed as a separate taxpayer and assessed on its own landholdings.

2. Bare Trust or Property Trust

Properties held via bare trusts (often used for LRBA loans) may still trigger land tax, depending on the state’s treatment of trusts.

Tip: In NSW and VIC, properties held in trust structures may be assessed at higher or separate rates, so declarations and proper trust registration are essential.

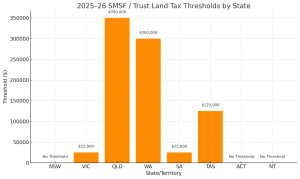

2025–26 Land Tax Rates by State and Territory (SMSF / Trust Thresholds)

| State/Territory | SMSF / Trust Threshold | Land Tax Rates (FY 2025–26) | Surcharge (if any) | Common Exemptions |

|---|---|---|---|---|

| NSW | $0 (no threshold for discretionary trusts) | $100 + 1.6% > $0; 2% > $6.571M | +2% for foreign owners | Farming land (no PPR for SMSFs) |

| VIC | $25,000 (for trusts) | 0.2%–2.55% (progressive) | +2% for foreign owners | Primary production land only |

| QLD | $350,000 (for trusts/SMSFs) | 1% > $350K, scaling up to 2.75% > $10M | None | Farming land (no PPR for SMSFs) |

| WA | $300,000 | $300 + 0.25%–2.67% | None | Farming land (no PPR for SMSFs) |

| SA | $25,000 (for trusts) | 0.5%–2.4% | None | Farming land only |

| TAS | $125,000 (as of 2024 update) | 0.55%–1.5% | None | Farming land only |

| ACT | No threshold (progressive from $1) | 0.54%–1.12% | None | PPR available to individuals only |

| NT | N/A | No land tax applies | N/A | N/A |

Important Notes for Trustees:

-

Principal Place of Residence (PPR) exemptions generally do not apply to SMSFs.

-

NSW and VIC apply no or low thresholds to trusts including SMSFs which means land tax applies from the first dollar of value.

-

QLD and WA offer comparatively higher thresholds, but aggregation rules may apply if property is held across multiple entities or related trusts.

Chart: Land Tax Rates Comparison Across States

Strategies to Reduce SMSF Land Tax

-

Diversify Property Holdings Across States

-

Each state has different thresholds. Splitting purchases reduces cumulative exposure.

-

-

Avoid High Land Values in a Single State

-

Try to purchase property under the threshold or across multiple legal entities.

-

-

Use Bare Trust or Company Structures Wisely

-

In some states, bare trusts may be taxed at higher rates unless disclosed early.

-

-

Claim Available Exemptions

-

If property is used for farming (primary production), check for land tax relief.

-

-

Plan Purchases Before Year-End Cut-Off

-

Most states assess land tax based on ownership as at 31 December.

-

Frequently Asked Questions

Q1. Does My SMSF Always Have to Pay Land Tax?

No. Your SMSF pays land tax only if the property value exceeds the tax-free threshold in that particular state.

Q2. Can I Structure My SMSF to Reduce Land Tax?

Yes. Using bare trusts or corporate trustees with properties in different states may reduce exposure. Always get legal and tax advice.

Q3. Is Land Tax Deductible in an SMSF?

Yes. Land tax is a deductible expense for your SMSF, reducing assessable income and tax liabilities.

Conclusion

Land tax is a significant cost consideration for any SMSF investing in property. Each Australian state and territory has different rules, and failing to plan can cost your fund thousands. Proper structuring, exemption claims, and state diversification can help you legally minimise land tax while remaining compliant. If you are unsure about your SMSF’s land tax exposure, speak to an SMSF specialist or property tax advisor before making a new investment.

Disclaimer

This article provides general information only and is not legal or tax advice. Always consult with a , lawyer, or financial advisor regarding your SMSF land tax obligations.