📑 Contents Why SMSF Death & Succession Planning Matters Key Tools for SMSF Death Planning 2.1 Binding Death Benefit Nominations (BDBNs) 2.2 Reversionary Pension Who Can Receive SMSF Death Benefits? Leaving Super to Your Children When to Review Your SMSF Succession Plan Trustee Considerations for Succession FAQs Final Thoughts Disclaimer SMSF Death benefit Planning for […]

📑 Contents

SMSF Death benefit Planning for SMSF Members:

When it comes to managing your SMSF death benefit planning, investing wisely is only one part of the strategy. Ensuring your loved ones are protected and your wishes are carried out after your passing is equally important. At My SMSF, we believe that robust death and succession planning is essential for every super fund.

This article explores your options, when and how often you should review your plans, and the implications of leaving benefits to both dependent and non-dependent beneficiaries, including your children.

Why SMSF Death benefit Planning Matters in an SMSF

An SMSF gives you control over your retirement savings, but with that control comes responsibility. Unlike public super funds, SMSFs require members and trustees to be proactive about how death benefits are handled. Without a clear plan, your superannuation savings could be distributed in a way that does not reflect your wishes and may result in unnecessary tax consequences for your beneficiaries.

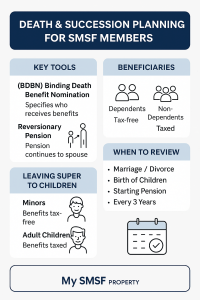

Key Tools for SMSF Death Benefit Planning

1. Binding Death Benefit Nominations (BDBNs)

A Binding Death Benefit Nomination is a legal document that directs your SMSF trustee to pay your death benefits to the person(s) you choose. My SMSF provides its clients with a free non lapsing Binding Nomination

Advantages:

-

Provides certainty over who receives your super.

-

Bypasses potential trustee discretion or conflict among family members.

-

Can reduce the chance of legal disputes or delays.

Important Notes:

-

BDBNs must be valid and up to date.

-

Many are lapsing and expire every three years unless renewed although non-lapsing nominations are possible in SMSFs if permitted by the trust deed.

2. Reversionary Pension

If you are already drawing a pension from your SMSF, you can nominate your spouse or another dependent to automatically continue receiving the pension upon your death. This is called a reversionary pension.

Advantages:

-

Keeps assets within the fund.

-

Avoids interruption to pension payments.

-

Often more tax-effective than a lump sum.

Who Can Receive Your SMSF Death Benefits?

Your SMSF can pay death benefits to the following:

Dependents (Tax-Effective Options):

-

Spouse (including de facto)

-

Children under 18

-

Financial dependents

-

Interdependent

Tax outcome: generally tax-free for these beneficiaries if paid as a lump sum or pension.

Warning: seek legal and financial advice, this is a very general explanation

Non-Dependents (Tax Consequences Apply):

-

Adult children over 18 who are not financially dependent.

-

Friends, siblings, or other relatives outside the “dependent” definition.

Tax-free component: Always tax-free to any beneficiary (dependant or non-dependant).

Taxable component splits into:

-

-

Taxed element: to a non-dependant, tax is 15% + Medicare levy (2%) when paid directly from the fund.

-

Untaxed element: to a non-dependant, tax is 30% + Medicare levy (2%) when paid directly from the fund. (Untaxed often arises from insurance proceeds or certain public-sector funds.)

-

Warning: Seek Advice, this is a simplistic explanation

Planning for Your Children

When embarking on SMSF Death Benefit planning, many SMSF members intend to leave some or all of their super to their children. If your kids are:

-

Minors: They qualify as dependents, and benefits are generally tax-free.

-

Adults (not financially dependent): Benefits are taxable, so strategic planning is essential.

Options to Consider:

-

Life insurance through your SMSF to cover expected taxes.

-

Transferring assets like property to children via testamentary trusts outside super.

-

Equalising inheritances through non-super assets.

When Should You Review Your SMSF Death Benefit Plan?

You should review your SMSF estate and succession planning:

| Life Event | What to Review |

|---|---|

| Marriage or Divorce | Update BDBNs and trust deed to reflect new relationships. |

| Birth of Children or Grandchildren | Consider tax impacts and potential financial dependency. |

| Starting a Pension | Decide on a reversionary beneficiary. |

| Major Asset Purchase (e.g. Property) | Ensure property fits into your long-term succession strategy. |

| Every 3 Years (or sooner) | Reconfirm nominations, re-evaluate tax outcomes, and update trustee roles. |

SMSF Trustee Considerations

If you are the sole member and trustee, it’s vital to ensure someone you trust can step in after your passing. Consider:

-

Appointing a legal personal representative (LPR) in your Will to act as trustee.

-

Updating the trust deed to allow for succession planning flexibility.

-

Ensuring your executor understands the SMSF’s rules and assets (particularly if it holds crypto, property, or gold).

Final Thoughts: Don’t Leave It to Chance

When reviewing your SMSF Death benefit planning, you should seek legal advice on all of your estate matters as they often tie into your SMFS Death benefit planning. We recommend scheduling a review annually or after major life events to ensure your strategy remains current and tax-effective.

Additional Resources:

- ATO Binding Nominations – ATO information

- My SMSF – Setup Steps and Nominations

❓ FAQs

1. What happens if I die without a Binding Death Benefit Nomination?

The SMSF trustee decides who receives your super, following superannuation law. This could lead to disputes or delays.

2. Can my adult children receive my SMSF tax-free?

No, adult children (unless financially dependent) pay tax on the taxable portion of your super.

3. How often should I review my SMSF nominations?

We recommend at least every 3 years or after major life changes like marriage, divorce, or having children.

Disclaimer

This article contains general information and is not personal financial or legal advice. SMSF succession planning should be tailored to your situation. Always consult a qualified adviser before acting.