Mortgage Budgeting Strategies to Rebalance Your Home Finances High inflation is not just a headline it hits home, literally, pun intended. When interest rates rise to combat inflation, your mortgage repayments, grocery bills, and utility costs can all climb. For Australian homeowners and SMSF members, we show you some mortgage budgeting strategies for Australian homeowners […]

Mortgage Budgeting Strategies to Rebalance Your Home Finances

High inflation is not just a headline it hits home, literally, pun intended. When interest rates rise to combat inflation, your mortgage repayments, grocery bills, and utility costs can all climb. For Australian homeowners and SMSF members, we show you some mortgage budgeting strategies for Australian homeowners and SMSF trustees.

Whether you are holding a property inside your SMSF or managing personal expenses, here’s how to navigate high inflation with confidence.

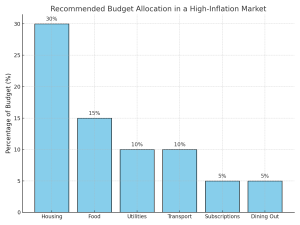

- Revisit and Realign Your Household Budget

Start by breaking down your essential expenses

- housing,

- food,

- utilities, and transport

Then look at discretionary spending

- subscriptions,

- dining out

- luxury items

Action Tip:

Use a budgeting app like ‘Cashrewards’ to track real-time spending. Set caps for non essential categories and commit to reviewing your budget monthly.

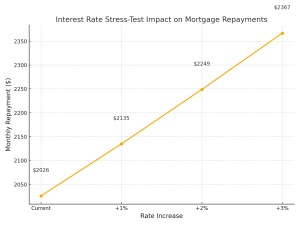

- Stress-Test Your Mortgage

If you’re on a variable-rate mortgage, each rate hike affects your repayments. If you are using an SMSF loan, you should model scenarios with interest rates 1–3% higher than your current rate.

Action Tip:

Use a mortgage calculator to see how much more you’d pay under different interest rate environments. Speak to your lender or broker to explore refinancing or switching to a fixed rate.

- Make Fortnightly Payments Instead of Monthly

This small shift results in an extra month’s payment each year. Over time, this reduces your interest and helps pay down your loan faster.

Action Tip:

Ask your lender if your home loan allows flexible repayment frequencies and if there are any fees associated with early payments.

- Build a Cash Buffer or Emergency Fund

With inflation driving up the cost of essentials, an emergency fund is your financial shock absorber. Aim for 3–6 months’ worth of expenses in an offset account (for mortgages) or high interest savings account.

Action Tip:

If you have an SMSF property loan, consider maintaining a liquidity buffer inside the fund to meet future interest or property costs.

- Look for Areas to Save or Renegotiate

High inflation forces everyone to reassess, from insurance premiums to utility bills.

Action Tip:

- Review your electricity, phone, and internet plans annually.

- Compare health and home insurance through comparison sites.

- Contact providers to ask for retention discounts, you may be surprised how often it works.

- Delay Major Purchases Unless Necessary

Inflation can inflate prices. If a large purchase (like a new car or kitchen renovation) if its not urgent, delay it. You could save significantly once inflation cools and supply chain pressures ease.

- Invest in Inflation Resilient Assets

For SMSF members, consider reallocating part of your portfolio into assets that historically perform well during inflationary periods, such as:

- Gold or precious metals

- Infrastructure funds

- Property with rising rental yields

- Index funds with inflation-linked securities

Speak to your licensed SMSF adviser or accountant to explore compliance-safe options within your fund.

- Reassess Insurance Within Super

Rising premiums and cost-of-living pressures can tempt members to cancel insurance held inside super. Instead, assess the value and relevance of your cover not just the cost.

Action Tip:

Ensure you’re not underinsured or paying for duplicate policies across retail and SMSF super accounts.

- Review and Consolidate Debts

If you have multiple loans or high-interest debts, consolidation may reduce your repayments. Just make sure you are not stretching your loan over a longer period and paying more interest overall.

Action Tip:

Look into balance transfer offers or talk to your broker about restructuring into one manageable loan.

- Seek Expert Guidance

During volatile periods, it’s more important than ever to get advice. Whether it is from a financial adviser, mortgage broker, or SMSF specialist, guidance based on your specific circumstances can save you thousands in the long run.

Final Thought

These mortgage budgeting strategies in Australia will help you stay in control even when interest rates rise. If you are a property owner or SMSF investor, taking the time to structure your budget can protect your wealth and reduce financial stress.

Stay proactive. Stay educated. And if you need help reviewing your SMSF property or mortgage strategy, get in touch with us at My SMSF.

Additional Resources:

- Money Smart Site: Budget Calculator

- My SMSF Calculators: SMSF Calculators

General Information Warning: This information is general in nature. You should seek financial advice before acting on the information in this article.