General transfer balance cap indexation on 1 July 2026 — and what it means for non-concessional contributions (NCCs) Published: 19 February 2026 (ATO) From 1 July 2026, the ATO will index the general transfer balance cap (TBC) by $100,000, lifting it from $2.0 million to $2.1 million. At the same time, the defined benefit income […]

General transfer balance cap indexation on 1 July 2026 — and what it means for non-concessional contributions (NCCs)

Published: 19 February 2026 (ATO)

From 1 July 2026, the ATO will index the general transfer balance cap (TBC) by $100,000, lifting it from $2.0 million to $2.1 million. At the same time, the defined benefit income cap (DBIC) will rise to $131,250 for 2026–27 (up from $125,000).

Most trustees think “TBC = pensions”. That’s correct,but for many SMSF members the bigger day-to-day impact is the flow-through into Total Super Balance (TSB) thresholds, because TSB determines:

-

whether you can make non-concessional contributions (NCCs) at all

-

whether you can access the bring-forward rule (2 or 3 years)

-

and several other super concessions

If you’ve been hovering around the old $2.0m line, the move to $2.1m can be the difference between “nil NCCs” and “back in the game” in 2026–27.

Contents

-

What’s changing on 1 July 2026

-

Personal transfer balance cap: why some people get less than $100k

-

The key point for contributions: TBC indexation lifts TSB thresholds

-

Expected NCC limits for 2026–27 (and the new bring-forward table)

-

Worked examples

-

Practical SMSF planning checklist before 30 June 2026

-

FAQs

-

Disclaimer

1) What’s changing on 1 July 2026

The headline numbers (ATO)

| Measure | 2025–26 | 2026–27 (from 1 July 2026) | Change |

|---|---|---|---|

| General transfer balance cap (TBC) | $2,000,000 | $2,100,000 | +$100,000 |

| Defined benefit income cap (DBIC) | $125,000 | $131,250 | +$6,250 |

Source: ATO SMSF newsroom

Why the ATO is pushing reporting before 1 July 2026

The ATO has encouraged funds and advisers to report transfer balance cap events as they occur, and as early as possible before 1 July 2026, because your personal TBC is calculated using events the ATO has received and processed.

SMSF takeaway: TBAR reporting isn’t “just admin”. Late or missing events can distort what the ATO thinks your cap position is when indexation lands.

2) Personal transfer balance cap: why some people won’t get the full $100,000 increase

A common trap is assuming everyone’s personal cap goes up by $100k.

In practice:

-

If you start your first retirement-phase income stream on/after 1 July 2026, you’ll generally have a $2.1m personal TBC.

-

If you already commenced a retirement-phase pension in the past, your personal increase is typically proportional, depending on how much of your cap you previously used.

Quick comparison table

| Concept | What it controls | Which “cap” matters most? |

|---|---|---|

| Personal transfer balance cap | How much you can move into retirement phase (pension) | Your personal TBC |

| NCC eligibility / bring-forward | Whether you can make after-tax contributions and how much | Your TSB thresholds (linked to the general TBC) |

That last line is the trustee “aha”: NCC rules link to general TBC via TSB thresholds — not your personal cap.

3) The key point for contributions: TBC indexation lifts TSB thresholds

The ATO’s note is clear: indexation of the general TBC has flow-through consequences for TSB thresholds, and TSB affects:

-

NCC cap and bring-forward

-

carry-forward concessional contributions

-

work-test exemption

-

spouse tax offset eligibility

-

government co-contributions

The “re-entry” effect (why $2.1m matters)

Under the 2025–26 framework, a TSB at/above $2.0m generally meant nil NCCs. From 2026–27, that “hard stop” moves up to $2.1m.

So a trustee sitting at, say, $2.03m at 30 June 2026 may shift from blocked to eligible in 2026–27 (subject to the rules).

4) Expected NCC limits for 2026–27 (and the new bring-forward table)

Expected cap indexation from 1 July 2026

Based on AWOTE/CPI outcomes reported by industry specialists, caps are expected to increase from 1 July 2026:

-

Concessional cap: $30,000 → $32,500

-

Non-concessional cap: $120,000 → $130,000

Bring-forward thresholds table (2026–27)

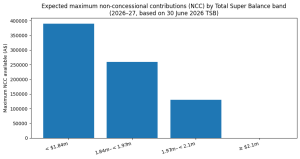

Heffron’s 26 Feb 2026 update sets out the 2026–27 thresholds (based on TSB at 30 June 2026):

| Your TSB at 30 June 2026 | NCC cap available in 2026–27 | What that means |

|---|---|---|

| ≥ $2.1m | $nil | No NCCs allowed |

| $1.97m to < $2.1m | $130,000 | 1 year only |

| $1.84m to < $1.97m | $260,000 | 2-year bring-forward |

| < $1.84m | $390,000 | 3-year bring-forward |

Two trustee-level rules that matter:

-

These bands are determined using TSB at 30 June 2026 (not your balance on the day you contribute).

-

The shift in the “nil NCC” line from $2.0m → $2.1m is the unlock for many members.

Chart: NCC capacity by TSB band (2026–27)

5) Worked examples: how TBC and TSB change your NCC cap

Example 1 — “Locked out, now back in”

Priya (62) has:

-

SMSF accumulation: $1.85m

-

Industry fund accumulation: $180k

-

TSB at 30 June 2026: $2.03m

Outcome (2026–27): Priya sits in the $1.97m–<$2.1m band → $130,000 NCC (no bring-forward).

Why it matters: Under the old $2.0m hard stop, this range was often “effectively nil”. Now she has a pathway for recontribution/estate planning or post-sale/inheritance contributions (subject to her circumstances).

Example 2 — Timing is everything (delay the bring-forward trigger)

Mark (60) has TSB $1.82m at 30 June 2026.

Outcome (2026–27): Under $1.84m → eligible to trigger 3-year bring-forward → up to $390,000.

Strategy lever: In a “cap-change year”, some members may prefer to avoid triggering bring-forward too early, and instead sequence contributions across June/July — but only if their 30 June 2026 TSB stays in the right band.

Example 3 — Personal TBC vs NCC eligibility (not the same test)

Helen (66) started an account-based pension years ago and has used her personal cap at that time. Her total super is now $2.05m (pension + accumulation).

Even if Helen’s personal TBC increase is limited, she may still be eligible for NCCs in 2026–27 provided her TSB at 30 June 2026 is below $2.1m.

Trustee lesson:

-

Personal TBC = pension transfer limit

-

TSB thresholds = NCC and bring-forward access

6) Practical SMSF planning checklist before 30 June 2026

| What to do | Why it matters | When |

|---|---|---|

| Estimate TSB at 30 June 2026 | This number controls your 2026–27 NCC options | Before 30 June 2026 |

| Stress-test the threshold bands ($1.84m / $1.97m / $2.1m) | Small valuation/market movements can change your NCC outcome | May–June 2026 |

| Check TBAR events are up to date | ATO wants TBC events reported early; it affects personal cap accuracy | Now → 30 June 2026 |

| Model June/July sequencing | In some cases, July 2026 contributions increase total available cap | Before triggering bring-forward |

7) FAQs

FAQ 1: Does the increase to $2.1m mean I can put $2.1m into pension phase?

Not automatically. The general cap becomes $2.1m, but your personal cap depends on your pension history and proportional indexation rules.

FAQ 2: Will the higher TBC increase my NCC cap?

Indirectly, yes. The higher general TBC lifts TSB thresholds, which can restore NCC eligibility or increase bring-forward access.

FAQ 3: If my personal TBC doesn’t increase much, can I still make NCCs?

Potentially yes. NCC eligibility is based on TSB thresholds linked to the general cap, not your personal cap.

Additional Information Links

- ATO – Transfer Balance Details

- My SMSF – Contact Us

8) Disclaimer

This article is general information only and is not financial or tax advice. Super outcomes depend on your circumstances (including age, contribution history, fund structure, pension status, reporting timing, and how the law applies to you). Before acting, consider personal advice from a licensed adviser and/or SMSF specialist accountant, and confirm balances/caps using ATO online services.