State of the Markets 2025 – What It Means for Your SMSF in 2026 State of the Markets 2025 – Snapshot for SMSF Trustees 2025 has been a year of transition for investors and SMSF trustees. Interest rates have fallen their peaks but remain high enough to bite. Australian property has stayed surprisingly resilient, U.S. […]

State of the Markets 2025 – What It Means for Your SMSF in 2026

State of the Markets 2025 – Snapshot for SMSF Trustees

2025 has been a year of transition for investors and SMSF trustees.

Interest rates have fallen their peaks but remain high enough to bite. Australian property has stayed surprisingly resilient, U.S. shares are being driven by AI-linked tech giants, while gold and Bitcoin have both delivered big moves and big headlines.

For SMSF trustees, the key question is simple: what does this mean for 2026 and for your retirement savings strategy?

2025 Market Overview – Key Asset Classes at a Glance

Use this section as a high-level briefing for clients before diving deeper.

Table – Key Markets Snapshot (Late 2025)

| Asset / Theme | 2025 Position (Approx.) | What’s Driving It | 2026 Watchpoint |

|---|---|---|---|

| Australian Property | National dwelling prices up ~4–6% over the year; new record highs in mid–high $800k median range. | Low listings, strong migration, earlier rate cuts. | Can borrowers handle repayments if unemployment rises or rates stay high? |

| Household Debt | Household debt ≈ 112–113% of GDP; debt-to-income ratios near record highs. | High mortgage balances and expensive housing. | Any shock to employment or rates transmits quickly through households. |

| Interest Rates | RBA cash rate at 3.60% (Nov 2025). | Sticky inflation and slowing growth. | How quickly can central banks cut without reigniting inflation? |

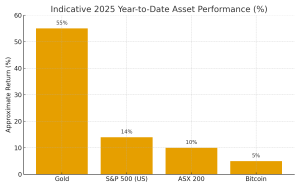

| ASX 200 | Trading near record highs around 8,500+ points; low double-digit gains versus late 2024. | Banks, miners and quality industrials. | Earnings resilience if global growth slows. |

| S&P 500 (U.S.) | Around 14% price return year-to-date in 2025, heavily led by AI-linked mega-caps. | AI and tech concentration. | Whether earnings justify premium valuations. |

| Gold | Spot gold around US$4,100/oz, up more than 50% over the year; strong central-bank demand. | Currency hedging, geopolitical risk, inflation concerns. | Forecasts suggesting an elevated 2026 average above US$4,000/oz. |

| Bitcoin | Fell from above US$120k to around the US$80k–90k range after a sharp November 2025 correction and ETF outflows. | Profit-taking, leverage washouts, institutional flows. | Whether ~US$80k holds as a new cycle “floor” or a deeper washout occurs. |

Australian Economy 2025 – Property, Debt and Interest Rates

Australian Property – Resilient but Less Affordable

In 2025, Australian property has continued to surprise on the upside:

-

National home values are up around 6% year-on-year to late 2025.

-

Median dwelling values are in the mid-$800,000s, with capital cities and land-constrained regions leading.

For SMSF trustees:

-

Quality residential property in high-demand areas remains a long-term wealth builder.

-

Cash flow matters more than ever – rising rents help, but higher interest costs can erode net yield.

-

Any property acquisition through an SMSF using an LRBA should be stress-tested under higher interest rates and conservative rental assumptions.

Household Debt – A Structural Risk for Australia

Australia remains one of the most indebted household sectors in the world:

-

Household debt is roughly 112–113% of GDP.

-

Debt-to-income ratios linger near record highs.

This matters for SMSF members because:

-

High mortgage costs and cost-of-living pressures may reduce contribution capacity.

-

Economic shocks (job loss, rate spikes) can quickly affect members’ broader financial position.

-

Investment strategies should assume that shocks move quickly through heavily indebted households.

Interest Rates – Off the Peak, Not Back to “Cheap Money”

The Reserve Bank of Australia has cut rates from their peak but left the cash rate at 3.60% in the second half of 2025.

For SMSFs:

-

Cash and term deposits now offer moderate yields and can play a meaningful defensive role.

-

However, cash alone is unlikely to deliver retirement outcomes, especially in accumulation phase.

-

Borrowing costs for SMSF property (including related-party loans) remain noticeably higher than the previous decade, demanding more conservative gearing.

Shares in 2025 – Australia vs U.S. Markets

Australian Shares – Income and Steady Growth

The S&P/ASX 200 has delivered solid returns:

-

Trading near record highs, supported by banks, miners and quality industrials.

-

Franked dividends remain a key attraction for SMSFs seeking income.

Key considerations:

-

Sector concentration remains a structural feature of the Australian market.

-

Many trustees use a blend of:

-

Broad market ETFs

-

Factor strategies (value, quality, equal-weight)

to improve diversification.

-

U.S. Shares – AI and Tech Lead the Market

In the U.S.:

-

The S&P 500 is up around 14% in 2025, driven largely by AI and mega-cap tech stocks.

-

The “S&P 493” (the rest of the index) has lagged these leaders.

For SMSFs:

-

U.S. exposure has been rewarding, but concentration risk is high.

-

A diversified global exposure (developed and emerging markets) is generally preferable to a narrow bet on a handful of tech names.

-

Currency moves between the AUD and USD will continue to add noise to returns.

Gold in 2025 – From Hedge to Core Allocation

Why Gold Has Been a Standout in 2025

Gold has been one of the strongest major assets this year:

-

Spot gold has traded around US$4,100/oz, significantly above prior peaks.

-

Central banks have been net buyers, using gold to diversify away from traditional reserve currencies.

-

Investors have turned to gold as a hedge against inflation, currency debasement and geopolitical risk.

Gold’s Role in an SMSF Portfolio

For SMSF trustees, a modest allocation to gold can:

-

Provide diversification when shares and property face cyclical pressure.

-

Act as a store of value in times of heightened geopolitical or financial risk.

-

Complement defensive assets like cash and short-duration bonds.

Many trustees consider a 5–10% allocation (depending on risk profile and age), implemented via:

-

Direct bullion (where permitted and practical), or

-

Gold ETFs and managed funds.

Bitcoin in 2025 – Volatility with Growing Institutional Interest

Bitcoin’s 2025 Rollercoaster

Bitcoin’s journey in 2025 has been dramatic:

-

Prices pushed above US$120,000 before falling sharply back into the US$80,000–90,000 range.

-

Record inflows into spot Bitcoin ETFs earlier in the year were followed by record outflows during the correction.

This highlights that:

-

Bitcoin remains highly volatile and should never be mistaken for a defensive asset.

-

Institutional adoption is increasing, but so too is the scale of leveraged and speculative trading.

How Bitcoin Fits (If at All) in an SMSF

For SMSFs that allow crypto:

-

Treat Bitcoin as a high-risk, satellite holding – not as the core of the portfolio.

-

Keep allocation sizes to low single digits of total SMSF assets for most trustees.

-

Ensure strict compliance and record-keeping:

-

Cold wallets in the fund’s name

-

Clear transaction histories and year-end valuations

-

Clear separation between personal and SMSF holdings

-

Any Bitcoin exposure should be documented in the investment strategy, with specific references to volatility, liquidity and risk management.

Investment Themes for SMSFs in 2026

Theme 1 – No Return to “Free Money”

Even with rate cuts:

-

The era of near-zero cash rates is unlikely to return in the foreseeable future.

-

Central banks are aiming for a new equilibrium where real rates are mildly positive.

Implications for SMSFs:

-

Cash and term deposits regain importance as part of the defensive allocation.

-

However, long-term retirement outcomes still rely on growth assets such as shares and property.

-

Gearing should be used carefully and conservatively.

Theme 2 – Scarcity and Real Assets

2025 has rewarded assets with scarcity and real-world utility:

-

Residential property in supply-constrained locations.

-

Gold as a monetary hedge.

-

Bitcoin as digital scarcity for those comfortable with its risk profile.

In 2026, many trustees will continue to favour:

-

Real assets (property, infrastructure, commodities).

-

Scarcity assets (gold, and in some cases Bitcoin) as partial hedges against fiat currency risk.

Theme 3 – Quality, Diversification and Resilience

Given how concentrated returns have been:

-

In a handful of U.S. tech stocks, and

-

In a few headline trades like gold and Bitcoin,

…it is crucial to focus on:

-

High-quality companies with strong balance sheets and persistent cash flows.

-

Diversification across regions, sectors and asset classes.

-

Building portfolios designed to survive bad years, not just chase the best performers of the last 12 months.

Practical Guidance for Savings and SMSF Strategy in 2026

Strengthen Your Personal Balance Sheet First

Before optimising your SMSF portfolio, consider:

-

Reducing non-deductible debt (credit cards, personal loans, home loans).

-

Building an emergency buffer of 6–12 months of living expenses, ideally in an offset or high-interest account.

-

Avoiding over-gearing, whether in personal names or inside the SMSF.

Use the Super System Deliberately

Inside your SMSF:

-

Make steady use of your concessional contributions cap, where affordable.

-

Consider non-concessional contributions if appropriate, to bring more assets into the super environment.

-

Keep fees down through transparent, fixed-fee SMSF administration and sensible investment product choices.

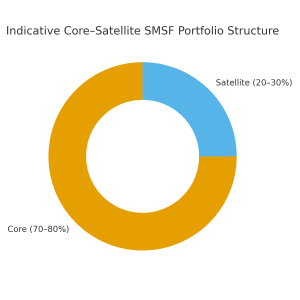

Example SMSF Asset Allocation Ranges (General information Only)

| Asset Class | Indicative Range (Accumulation Phase) | Role in Portfolio |

|---|---|---|

| Australian & Global Shares | 40–55% | Growth, dividends, franking credits. |

| Property (Direct / Listed) | 15–30% | Income, growth, partial inflation hedge. |

| Defensive (Cash, TDs, Bonds) | 10–25% | Liquidity, capital preservation, risk management. |

| Gold / Precious Metals | 5–10% | Hedge against inflation, currency and systemic risk. |

| Bitcoin / Approved Crypto | 0–5% (up to 10% for some profiles) | High-risk satellite exposure to digital scarcity. |

Note: These ranges are illustrative only and not personal advice. Every SMSF is different.

Savings and Risk Priorities for 2026

| Priority | 2026 Habit / Target | Why It Matters |

|---|---|---|

| Emergency buffer | 6–12 months living expenses | Reduces pressure to sell assets in downturns. |

| Concessional contributions | Use most/all of concessional cap where possible | Tax-effective way to grow retirement savings. |

| Debt reduction | Extra repayments on non-deductible debt | Improves resilience to rate or income shocks. |

| Regular investing in SMSF | Monthly or quarterly purchases | Smooths market volatility via dollar-cost averaging. |

| Annual investment strategy review | Formal review and minute each year | Keeps fund aligned with members’ needs and risk. |

FAQs – SMSFs, Markets and 2026 Strategy

Is 2026 a bad time to start an SMSF?

Not necessarily. The decision should focus on:

-

Whether you meet SMSF suitability criteria (balance, time, knowledge), and

-

Whether you have a clear, diversified long-term strategy.

You can mitigate market-timing risk by gradually investing over time instead of investing everything at once.

Should my SMSF buy property now or wait?

For SMSFs, property decisions should be guided more by:

-

Your fund’s investment strategy,

-

Values of property differs, in each state. The cycle of boom and bust varies from State to state, so its well worth speaking to a qualified property investment advisor. Member ages and retirement timelines are important SMSF considerations

-

Cash flow capacity under higher rates – do you 3% – 5% servicing stress test

than by trying to pick the exact bottom or top of the property cycle.

How much gold or Bitcoin should an SMSF hold?

There is no universal answer, but many trustees who include these assets:

-

Keep gold in the 5–10% range, and

-

Keep Bitcoin in low single digits of total SMSF assets.

The key is to ensure the allocation is:

-

Clearly documented in the investment strategy, and

-

Small enough that a severe drawdown does not jeopardise the fund’s core retirement goal.

Should I move everything to cash if I expect a crash?

A 100% cash position can be appropriate only in very specific circumstances (e.g. near-term drawdowns with surplus capital). For most trustees, it may reduce long-term returns significantly.

A more robust approach is to:

-

Maintain a sensible defensive allocation (cash and high-quality bonds).

-

Rebalance periodically instead of trying to jump entirely in or out of markets.

How often should I update my SMSF investment strategy?

Best practice:

-

Review annually, and

-

Update whenever there is a material change in:

-

Member circumstances,

-

Contribution patterns,

-

Asset mix (e.g. adding crypto or direct property), or

-

Risk tolerance.

-

Auditors and the ATO expect your investment strategy to reflect your actual investments.

Disclaimer for SMSF Investors

This article has been prepared for general information only for My SMSF clients and prospective clients. It:

-

Does not take into account your objectives, financial situation or needs.

-

Is not personal financial product advice, tax advice or legal advice.

-

Should not be relied upon to make investment or superannuation decisions without further advice.

Market prices, interest rates and data are approximate and based on information available as at 25 November 2025. Investment markets can change rapidly. Past performance is not a reliable indicator of future performance. Crypto assets such as Bitcoin are highly volatile and can result in substantial loss of capital.

Before acting on this information, you should consider its appropriateness in light of your circumstances and, where appropriate, seek advice from:

-

A licensed financial adviser

-

A registered tax agent

-

An SMSF specialist or legal professional

Further Reading and External Resources

-

Housing & Household Debt

-

Sharemarkets

-

Gold and Bitcoin

-

My SMSF Services